What to Look for in a Home Inspector

To avoid any disastrous surprises after purchasing a home, it’s highly recommended that you hire a quality home inspector. Additionally, it’s best practice to choose a home inspector before you make an offer on a home, as you’ll likely need to move quickly once an offer is submitted.

To avoid any disastrous surprises after purchasing a home, it’s highly recommended that you hire a quality home inspector. Additionally, it’s best practice to choose a home inspector before you make an offer on a home, as you’ll likely need to move quickly once an offer is submitted.

But what should you look for in a home inspector? Our checklist below should help you find a home inspector you can rely on.

1. Certification

There are 2 major professional organizations for home inspectors, American Society of Home Inspectors (ASHI) and the International Association of Certified Home Inspectors (InterNACHI). On the above websites, you can search for any home inspector to see if they’re certified by each respective organization. Certification by either of these organizations is not a requirement to be a professional home inspector. In fact, some states don’t even require home inspectors to be licensed at the state level.

That being said, if an inspector is certified by either of the above organizations, it’s a good indicator that the inspector is serious about their work. These organizations require rigorous processes to maintain certification, typically much more than is required at the state level.

Speaking of state certifications, the ASHI website includes a feature to see the applicable home inspection requirements in your state. If the state does require inspectors to be licensed, the state agency’s website will typically include a search tool to verify that your inspector’s license is current.

2. A Normal Price

If you’re interviewing multiple home inspectors, it could be tempting to go with whoever has the lowest price. However, if one home inspector’s prices are significantly lower than everyone else you speak to, that should be a red flag that something is wrong. A qualified, experienced home inspector is not typically going to charge bargain barrel prices. That doesn’t necessarily mean that you should look for the highest price either. Just be wary of any deal that sounds too good to be true, because it probably is.

3. Experience

As with most professions, it’s usually a good sign if a home inspector has plenty of experience. That experience can come in different forms; many home inspectors have background experience in construction or as a contractor, which is a positive. At the same time, that experience is not necessarily a substitute for years of experience working as a home inspector.

Keep in mind that experience alone doesn’t necessarily indicate that someone will do the best job. You may like your introductory call with a more novice home inspector who checks off the rest of your boxes. Plus, if a novice home inspector is certified by an organization like ASHI, they’ve likely been mentored by more experienced inspectors as a requirement of their certification.

4. Specialization

If you’re still shopping for a home, you may not know what type of specialty experience you will need. However, if you are able to narrow down specific types of experience you’ll need (such as new construction, or if you know you’re purchasing an older home), that should help find the right inspector for the job.

This type of specialization is important when it comes to non-typical issues that a general home inspection may not always need. For example, if you’re purchasing a much older home, you may want someone with experience testing for lead.

5. References

It may not occur to you to request references from a few past customers, but this should not be a surprise to the home inspector. You’ll want to ask these customers about the inspection process, how well the inspector communicated (before, during, and after the job), and how comprehensive the inspection report was.

Other resources are your state government website and the Better Business Bureau (BBB). You can look for any complaints about the home inspector and see if any disciplinary actions were taken against them in the past.

6. Insurance

Make sure your home inspector has liability insurance. Why is this important? Because on the off chance something happens to damage the home during inspection, the seller could potentially take legal action against you! Although this is rare, the cost could be substantial. Your home inspector’s liability insurance will ensure that you don’t end up paying for any accidental mishaps.

They may also have Errors and Omissions (E&O) insurance. This covers the inspector, and yourself, if they miss something big that should have been caught during the inspection. If an experienced home inspector does their job, this shouldn’t be an issue, but it’s still good to know they have it.

7. They Want You to Be There!

An experienced home inspector will encourage home buyers to be there for the inspection. If this is not possible, they’ll likely ask that you at least show up at the end to review the inspection report together. If a home inspector seems indifferent to you being there for the inspection, or worse, actively suggests that you not be there, that should be a major indicator that something is wrong.

By our Preferred Vendor, Choice Home Warranty.

For Additional Blog Content, Click Here!

Demand for vacation homes now outpacing primary homes: Redfin

Vacation-home demand is the highest it’s been in a year and just below a record 90% gain in demand tallied in September 2020, according to data released Thursday by Redfin.

Vacation-home demand is the highest it’s been in a year and just below a record 90% gain in demand tallied in September 2020, according to data released Thursday by Redfin.In January, vacation-home demand soared to the highest it’s been in a year and just below a record 90 percent gain in demand tallied in September 2020.

The popularity in second homes is so great that it’s actually outpacing demand for primary homes, which was up only 42 percent from pre-pandemic rates as of January.

Redfin gathered demand levels for this report by analyzing residential mortgage-rate lock data.

3 Key Differences Between Real Real Estate and Metaverse Real Estate

We’ve all heard of and understand what the metaverse is, right? Good for you if you answered yes. If you’re like me and over the age of 40 and/or not inclined to follow technology’s rapidly evolving pace, your answer was probably no. According to my extensive (not true) research (I typed in the Duck Duck Go search bar), a metaverse is a network of 3D virtual worlds focused on social connection. And it’s not just the wave of the future, it’s here.

We’ve all heard of and understand what the metaverse is, right? Good for you if you answered yes. If you’re like me and over the age of 40 and/or not inclined to follow technology’s rapidly evolving pace, your answer was probably no. According to my extensive (not true) research (I typed in the Duck Duck Go search bar), a metaverse is a network of 3D virtual worlds focused on social connection. And it’s not just the wave of the future, it’s here.

Some key takeaways to consider in purchasing virtual real estate vs. *real real estate…

What Currency To Use

Metaverse– You still need money, but in the metaverse you pay with crypto currency out of a digital wallet. But not all buying platforms accept all forms of crypto so you may be forced to invest in a speculative form that may or may not stick around and every crypto coin has its own value independent of others (not confusing at all), plus if you forget the ‘seed phrase’ you’re assigned when your wallet is opened it is almost impossible to retrieve it which means you have lost your virtual wallet with real assets in it. Like, gone.

Reality– When you buy real real estate, you’ll use your money (electronically withdrawn from a bank insured by the FDIC) in combination with a lender’s money if you get a loan. No need to worry about what kind of money, if it’s American currency and you’re buying real estate on American soil, you’re good. And if you forget your password, you can pretty easily retrieve it.

How To Find Property For Sale

Metaverse- As of now, there are not virtual Realtors to help you find virtual real estate so you will either do your own extensive research (and it is extensive) before buying your property (oh my goodness be sure you understand the real world asking price of the properties you’re interested in since crypto coins valuations vary) directly from a specific platform, or you can go through a third-party platform that offer buying and selling opportunities. You will have the ability to view what it is you’re interested in purchasing including nearby amenities as well as neighbors. That’s neat.

Reality- Hopefully you have employed the services of a qualified and reputable real estate agent who will listen to your wants and needs and initiate a search based off of your criteria via whatever online listing database is utilized in your neck of the woods. You will then start touring properties you like together and the agent will be able to educate you on the surrounding areas, schools, shopping, amenities, etc. You may even wave to a potential future neighbor or two. Here’s where a big difference comes into play. These future neighbors may provide cups of sugar for you in a pinch or even dare I say it, an actual physical friendship.

From Offer to Closing

Metaverse– Well, hands down for speed and ease, the process of making an offer and closing in the metaverse is much easier and quicker, but not as secure. Depending on which platform you’re buying from, you either make an offer on the land you want and it’s accepted or rejected, or even simpler, you click it and buy it with the cryptocurrency in your online wallet. No appraisals yet as this is all still highly speculative and valuations can fluctuate rapidly. Remember not to lose your digital wallet where you store your NFTs because there is no other way to retrieve your NFT title. And one more small detail, if a metaverse platform devolves and goes offline, so does your NFT real estate investment.

Reality– In the real world of course, especially now in this extremely tight seller’s market, the process can be much lengthier and somewhat draining emotionally if you are finding yourself competing with other buyers, but in the long run your purchase will be more secure. If you are getting a loan there will be an appraisal as the bank wants to insure the property is worth what you’re buying it for which alleviates a large portion of speculative risk. You will then head to a closing attorney’s office where you get the title after signing a ton of paperwork and paying the down payment. Here comes the best part, if the bank goes out of business, your asset doesn’t disappear, your mortgage just goes to a different lending institution. Oh, and of course you have physical land that you can go have a picnic on or actually build a house on. That’s the best best part.

Hopefully I’ve given you a little insight into the new world of metaverse real estate. I’m still learning myself and it’s a tad overwhelming. But if you’re interested in buying or selling physical land or an actual home, that doesn’t overwhelm me at all, in fact I love it. It would be an honor to serve you with any of your real real estate needs.

By Holly A. Morris, Realtor

The Meridian Real Estate Group

*For the sake of this article real real estate refers to land or property that is tangible to our senses in the physical world. There is an argument to be made that metaverse real estate is real too despite not being tangible.

For Additional Blog Content, Click Here!

Florida Home Listed For $650K In Proof-Of-Concept Crypto Auction

Ownership of the home will be transferred using a unique blockchain token — known as an NFT — that can be held in a crypto wallet.

An international property startup is launching a way to store U.S. home titles in a crypto wallet in the hopes that this process can be scaled to drive a large number of blockchain-based real estate transactions.

The company, Propy, is currently helping sell an investment property in the Florida city of Gulfport, near St. Petersburg. The 2,164-square-foot property has five bedrooms and is currently listed for $650,000.

To facilitate this type of transaction, Propy creates a limited liability company that owns the property. Ownership of that LLC will be tied to the owner of a unique blockchain token known as an NFT.

Through this setup, buyers will be able to purchase these NFTs — and by extension their LLCs, and the properties themselves — through a cryptocurrency transaction.

The seller is a real estate and cryptocurrency investor named Leslie Alessandra, according to the listing on Propy. She’s hired an agent from Heckler Realty Group to represent her. Propy says it has been assigned to create the NFT and auction it off.

The home is also listed on the MLS, according to its page on Zillow. The overview doesn’t mention the NFT process or Propy, describing the home as an “auction property.”

The company plans to hold the auction for this property on Feb. 8, Techcrunch reports. Signups for the auction are taking place on the listing page on Propy’s website.

To get in on the auction, prospective buyers are being asked to sign up from the listing page on Propy’s website.

The home’s list price of $650,000 is on the higher side of prices in the neighborhood. Zillow’s estimates for home values on similar sized lots on the same block range from $250,000 to $640,000.

If these NFT-assisted transactions start to take off, Propy anticipates the early use cases will focus primarily on so-called “collectible” properties.

“Trophy real estate owned by celebrities, or in prime location, or with unique digital art and architecture can be regarded as a collectible,” Propy said on the listing page. “The level of pride of ownership is very high, and the purchased price is almost irrespective of the trading potential of the property, just like with other collectibles.”

Propy had previously sold an apartment in Ukraine through a similar process.

At an Inman Connect Now session in June, Propy CEO Natalia Karayaneva said she wanted to make agents a party to this process.

“We’re very ambitious in the company that this can potentially transform the industry and transform the paradigm of home ownership,” Karayaneva said at the time. “We see that we can empower … agents to transact faster and make their customer look at the agent with more satisfaction.”

Thank you www.Inman.com for this article. For more articles like this, Click Here.

For Additional Blog Content, Click Here!

What crypto, NFTs and the rest mean for real estate

Where will you live when we’re all in the metaverse? Putting the ‘real’ back in real estate.

Real estate agents are selling property in the metaverse. Buyers are purchasing traditional homes with cryptocurrency. Companies are creating non-fungible tokens (NFTs) as digital titles for real properties.

How can you wrap your head around all of these technologies in a way that’s simple and pragmatic? I’m not a software engineer and no expert in crypto. I’ve read enough in this space to give you explanations that techies will probably hate.

But we’re just here to understand the business, not the technology protocols. Let’s talk about these new phenomena without the technical lingo and focus on what they mean in practice.

Under all is the land

Supply and demand: They define how real estate valuations rise and fall. Real property’s finite availability, its scarcity, underpins its value.

Does this scarcity exist in digital worlds? Do digital properties increase in value if a digital title can be purchased for them? Is purchasing these digital assets, or advising others to, a smart decision?

We’re going to look at the hype, the hope, and the skepticism. Let’s get down to brass tacks: what’s the new oil and what’s just snake oil?

The news headlines are mystifying. People are buying digital property rights on the internet. They’ve paid over $1 million for items like:

Virtual property in online cities

“The world’s gone mad,” you might say. But maybe it’s no madder than it’s ever been. Why would people pay so much for items which don’t exist in physical form? Potential profits, ego, excitement – is it all that different than a bet on a football game, the purchase of a vacation, or buying the bar a round of drinks?

What can’t be denied is that there’s a current demand for these digital assets. And demand generates money. Who makes the money, and how long that demand lasts, are the questions at hand in the metaverse.

The metaverse

The metaverse is often portrayed as a fully virtual world, but there are many degrees of metaverse. Remember Google Glass, the eyeglasses that displayed information in the lenses as you traversed the physical universe? You’ve seen a metaverse. Have you created an avatar in a game and interacted with others online? Metaverse.

You have connections on Facebook and you share friendships and emotions with them. This is just one component of the metaverse, and it’s not new. What is new are the deeper and more immersive versions of metaverses that we’re seeing today.

These digital experiences are different from your fully physical experiences, but they’re still undeniably real. Whether it’s a full 3D virtual reality experience or a video call on FaceTime, you’ve been experiencing levels of what people are now calling the metaverse for a long time.

NFTs: non-fungible tokens (Don’t quit reading!)

A token can be a “title” for ownership of something. A property title says you own real estate. A Chuck E Cheese token says you own the rights to play one game. A digital token says you own the right to something identified in a digital contract.

Fungible just means identical things can be exchanged for each other. Two Chuck E Cheese tokens are fungible. Two $1 bills are fungible.

Non-fungible things are unique. Each home on your block is non-fungible. Every condo in a building is non-fungible. There are fundamentally different location features of each.

Tokens transferring real estate

So a non-fungible token says you own the rights to something unique. And, yes, ownership of real estate can potentially be transferred with an NFT, in specific cases.

While the actual title to real property is governed by your local county or municipality in the U.S., you can create an LLC that legally owns a property. So you can also create an NFT that owns the LLC, and you can sell/buy/trade it. It’s been done by TechCrunch Founder Michael Arrington and CEO of Propy, Natalia Karayaneva.

Whether it’s a digital picture or an LLC for a piece of property, an NFT can prove your ownership. Just because you own it, doesn’t mean it’s worth anything. Let’s be honest, people buying ape pictures for thousands of dollars are probably going to regret it later.

But trading tokens that govern the ownership of real property is serious business. The environment is currently the Wild West, and the government will make its way into the conversation at some point. Remember that in most areas, property title transfer taxes on real estate sales are major funding sources for government projects. But there’s no government transfer tax guaranteed on an NFT sale. Uncle Sam’s going to come for his cut when he’s out of money to build roads.

But for now, there’s a lot of blue ocean in the viewfinder. New digital means to move property are, without question, preferable to today’s paper-and-stamp practices that still exist in many parts of the U.S.

Cryptocurrency

Cryptocurrency uses cryptography technology to create potentially valuable digital coins. They’re valuable today because people have created demand for them and will use “real” government-backed fiat currencies to buy them.

Bitcoin, Ether, Dogecoin … you can actually buy and sell things with them. It’s an extremely slow, expensive, and clunky experience to transact with them today, but there is the potential of more utility. Newer technologies with better experiences are being built alongside and on top of the current incumbents.

Bitcoin at Starbucks

Will cryptocurrencies become popular, broadly used currencies in everyday business? It’s difficult to say. Governments have, by and large, not played their inevitable cards on crypto yet. Today, it’s mostly people who are already deeply embedded in crypto enthusiasm that are buying items with them.

The only people I personally know who spend cryptocurrencies regularly today are using them to purchase other crypto assets or evade government detection – no joke. They’re sending money back to their family in foreign countries and don’t want the government to take a slice.

And those crypto real estate purchases we hear so much about: they’re mostly agents hyping a transaction where a buyer sells off crypto to pay in dollars for a home. There are platforms now, though, where a true crypto-for-title transaction can take place. They’re still rare.

Web3: A truly decentralized digital world

People are talking about Web3, the purported third major life cycle of the web. The vision of Web3 is that governments and huge corporations would no longer control our digital experiences. Instead, individuals could own and control their own data and destiny on a decentralized network by the people, for the people. Imagine a web where everyone is connected to everyone else but there’s no big platform that everyone is forced to connect with to get some desired digital experience.

Decentralization, in its purest form, does give power to individual contributors, but its complexity makes it expensive to do well. So true decentralization is actually rare across the spectrum of topics we’re covering. There are for-profit companies centralizing services to make them more easily accessible to consumers. Corporations still control almost everything today as far as consumers are concerned.

Blockchain (I Promise This Won’t Hurt)

Blockchain technology is at the root of most of these potential innovations (but not all). We don’t need to spend a lot of time on it, except for knowing that it creates distributed systems, which can have a central authority or be fully decentralized. It’s not hype, though it is sometimes overhyped.

You can imagine it as similar to how you use Google Docs to allow many people to edit a document at the same time on the web. They all have a record of what the document looks like now. They all have the ability to look at the history of all changes made by all participants on the document and that history is stored on Google’s servers, the central authority.

Imagine now if Google Docs was turned into open-source software: we’ll call it Boogle. Everyone installs Boogle on their own computer and they all connect to each other directly across the web without Google in charge anymore. This is decentralization.

If every person was constantly downloading the state of the document on their personal computer, they could always look back at the historical record of who changed what on their own device. No individual could hide what had happened in the historical records. Everyone is an owner of the immutable (unchangeable) truth.

This is essentially how blockchain works. Each node (computer) on the network has its own copy of the ledger (transaction record) and they all share updates with one another. One node can’t change history without the others knowing and agreeing.

Blockchains of many colors

So a cryptocurrency like Bitcoin operates a decentralized system where all users are in control. But blockchains can also be private, permissioned, tightly controlled networks.

For example, the Real Estate Standards Organization (RESO) is analyzing a model where every MLS in the country could contribute to a national Unique Licensee Identifier service via their own nodes on a blockchain network. This kind of service doesn’t exist in the U.S. today, as state agencies keep their own broker/agent license records and do not collaborate with one another. Agents who work and live in multiple states have disjointed records across MLSs, associations, brokerages, and vendors.

In a distributed ULI model, each node would be able to submit new license data and receive updates from the system. The MLSs could maintain some independence on their own systems while the central organization would be the overseeing data cop to ensure accuracy in distributed updates. Each MLS would know that nothing was being changed by the central authority without their knowledge as they’d have an unchangeable copy of all historical events.

Blockchains can be used by traditional companies in highly controlled environments, as well as in fully decentralized services. There are many different blockchains.

How sticky is your web?

Location, location, location: in real estate, proximity to high-demand amenities creates value. A property is networked to things based on its location: property structures, nearby schools, high-speed internet, beaches, employers, family members and more. For each individual, this network has an effect that influences what value they put on that piece of real estate. The more value the network provides to the buyer, the more they’ll pay.

These network effects are the key element to the value of digital assets, though focused on the people in your network. You might hate Facebook, but you can’t leave because your cousins put their new baby pictures there. Ancestry.com draws its users back over and over because more of their family continues to join, thereby improving the service’s value.

People continue buying iPhones for many reasons, one being that group messages with friends and family break when the only non-iPhone user responds with a message of the wrong color bubble. Your human network is sticky, and it creates lock-in for the products that hold it.

It’s important to think about the stickiness of these network effects when evaluating digital assets’ long-term value. Will people stay interested in them and for how long? Without physical assets attached, their entire value is based on the digital demand of humans, which can be a finicky thing.

Your metaverse neighbor: Snoop Dogg

So back to “real estate” in the metaverse: digital neighborhoods and cities are being built.

The demand for digital items is real. My kids buy video game logos and specialty wheels with their allowance to impress complete strangers playing online somewhere across the world. Digital property is, without a doubt, valuable.

Metaverse property has supply and demand repercussions like the physical world, except that supply in the metaverse is completely arbitrary and controlled by creators of software, while supply of physical real estate is constrained by geography, materials, labor, and government regulation.

When someone buys the lot in Decentraland next to Snoop Dogg for $1 million, maybe they’re crazy. But maybe they’re just making a bet on demand. If metaverse traffic flocks to Snoop’s block, the ability to leverage that high profile location could be lucrative: advertising on digital billboards, for example, could be profitable for a person with a plot of “land” in the right location.

Agents rush in, as they always do

Some agents are promoting the specious link between real property and digital land sales. Should real estate pros be giving advice to consumers about buying digital property? Probably no more than your Bitcoin maximalist cousin should. At a minimum, the ethical implications of purporting to have metaverse expertise via a real property brokerage license loom large.

There’s also a need to abide by securities sales and anti-money laundering laws. Just ask RE Consortia’s CEO, Teresa Grobecker, who consults on the intersection of law and distributed ledger technology. Not just anyone can sell investments to the public. Caution is warranted at this stage.

It ain’t real estate, but it is a gold rush. Remember who gets rich in physical gold rushes? It’s more pick and shovel salesmen than prospectors. There’s money to be made in the metaverse property game, but if the bottom falls out, there’s no land to land on.

Who Can You Believe?

Jack Dorsey, recently departed CEO of Twitter, has been working with his successor to incorporate decentralization elements onto the platform. He’s also CEO of payment company Square, which he renamed Block (chain). Dorsey says there’s nothing more important to work on in his lifetime than Bitcoin.

Elon Musk publicly touts his investments in Ethereum and Dogecoin. Jack Black, Eminem, Rob Gronkowski, Martha Stewart, Shaquille O’Neal and Mark Cuban have all sold NFTs. If you’re looking for successful, rich, famous or brilliant people to substantiate a belief in the future of decentralization and metaverse valuations, they’re not hard to find.

They might be right. The valuations for these bets could go to the moon. They could also melt down to nothing as the little guys are the last ones holding the bag. Successful people often famously don’t know any better than you do.

“The idea of a personal communicator in every pocket is nothing more than a pipe-dream fueled by greed.” Andy Grove, CEO of Intel, 1992.

“There is no chance of the iPhone ever gaining significant market share.” Steve Ballmer, CEO of Microsoft, 2007.

“Subscription models for music are bankrupt. I think you could make the Second Coming of Jesus himself available on subscription and it wouldn’t be successful.” Steve Jobs, CEO of Apple, 2003.

Finding the Balance

At this stage of the web’s evolution, it’s probably better to not have all the answers. The bets you make on metaverse properties or NFTs are speculative and there’s no reason to label them anything else.

There are substantial reasons to be a skeptic when it comes to comparing digital property to physical real estate. There are significant concerns about the government’s future scrutiny of investments in untaxed and unregulated securities and property transfers. This isn’t a game, and the government always gets its bite.

There are echoes of past financial frenzies where the rich and powerful got out early and the average Joes were left having evaporated their retirement savings. In addition, the unsustainable energy crisis that crypto technologies could inflict on the world are not to be ignored.

But it would be inadvisable, also, to dismiss the possibility that these new (and old) technologies could become critical utilities in our lifetimes. Many of the world’s most valuable companies only produce digital products. Video calls from across the globe on your mobile phone are an everyday thing today but were science fiction not so long ago.

This brave new world is filled with the same innovators, evangelists, hucksters and scam artists as the old one. Real estate professionals who intend to do business in this space should be explicit about the risks involved. This isn’t investment in real property, and it’s not a game where everyone wins. Sometimes fortune favors the bold. But for every Amazon, there’s a pets.com.

Carpe diem, caveat emptor.

Thank you www.Inman.com for this article. For more articles like this, Click Here.

For Additional Blog Content, Click Here!

Out-of-towners are causing home prices to soar in relocation hotspots

Prices are up as high as 30% in some relocation hotspots across the Sun Belt, where 9 of the 10 most popular US relocation destinations are, according to a report from Redfin released Monday.

Prices are up as high as 30% in some relocation hotspots across the Sun Belt, where 9 of the 10 most popular US relocation destinations are, according to a report from Redfin released Monday.Prices are up as high as 30 percent in some relocation hotspots across the United States Sun Belt — where nine of the 10 most popular relocation destinations are — pricing out locals and aspiring relocators alike, according to a new report from the online brokerage Redfin.

“Moving across the country is now easier for many Americans, thanks to remote work. That cultural shift is here to stay,” said Redfin Deputy Chief Economist Taylor Marr. “What’s changing is the affordability of the most popular destinations. Some locals, particularly renters who aren’t able to take advantage of rising home values, are getting priced out of places like Phoenix and Austin as the cost of housing and other goods and services go up.”

Inman Connect

Secure your tickets now for in-person & digital events!

Inman Top 5: The biggest stories of the week of Jan. 28-Feb. 3, 2022

You’re invited to Inman Connect’s 25th anniversary celebration

Introducing the 2022 Inman Global Ambassador Team

In Phoenix, the typical home sold for 28 percent higher in December than it did a year ago — well above the national average of 15 percent — while the average monthly rent price increased by 26 percent year over year. Consumer goods are also rising higher in relocation destinations, with an influx of new residents driving up inflation, according to a separate Redfin report.

Part of the price growth is driven by out-of-towners with larger budgets entering the market.

“Sellers are listing their homes at higher prices than ever before, partly because of huge demand in the last year from out-of-towners,” Austin Redfin agent Barb Cooper said in a statement.“I recently had a couple looking for a 2,000-square-foot home anywhere in the Austin area for under $300,000. I had to tell them it doesn’t exist.”

During the same period, all three cities saw the number of homes on the market decreased significantly. The amount of homes for sale decreased in Phoenix by 18.6 percent between 2020 and 2021, by 27.6 percent in Dallas, and by 29 percent in Orlando, according to Redfin.

“New construction tends to be robust in sprawling Sun Belt cities, and local governments ought to continue to prioritize building new homes to keep up with ongoing demand,” he said.

Sorry to burst your bubble, but we’re not in one, housing experts say

Today’s rising home prices and a persistent seller’s market differ from the 2007 housing bubble in a few key ways, economists told Inman. In short, don’t expect bubbles bursting anytime soon.

Today’s rising home prices and a persistent seller’s market differ from the 2007 housing bubble in a few key ways, economists told Inman. In short, don’t expect bubbles bursting anytime soon.It’s hard not to look at the unprecedented territory of the U.S. post-COVID housing market with a twinge of fear that the country is returning to conditions that existed before the collapse around the Great Recession.

“I was thinking, ‘What is really a bubble?’” said Selma Hepp, chief economist of CoreLogic. “There is no firm definition of a bubble.”

“To some people, high appreciation is going to be a bubble. To others it’s high speculation,” Hepp said. “Generally among economists we think when there is an increase in speculation, when people are buying based on expectation of appreciation as opposed to that need for housing, that’s when we could be in a bubble.”

In a way, the pandemic may have led buyers who ordinarily might have purchased a first or second home in a few years to do so much sooner.

“One question we don’t know for sure is how many people moved forward to buy a house because of the stimulus and low interest rates that they would have bought this year or next year,” said Doug Duncan, chief economist at Fannie Mae.

That expedited purchasing might not make it any easier for those who are getting squeezed out of entering the market for the first time.

“Everybody is going to have their own mindset and excuses to do or not to” buy, said Kyle Alberto, an agent with Porchlight in San Diego. “I just explain [that] buying now versus holding off and waiting for a bubble to burst is likely going to put you in a place where you’re paying the same price or more but at a much larger interest rate.”

There are a few things that make the market’s ongoing ramp up fundamentally different this time around.

More recently, the market has been driven by much healthier, fixed-rate and 30-year mortgages that give owners certainty after buying.

“We have much stronger borrowers [and] less risky loan products,” said Nicole Bachaud, a Zillow economist. “The vast majority of buyers are getting 30-year fixed mortgages … If you lock in a 30-year mortgage your monthly payment is not going to be changing.”

While that rate is rising and expected to keep climbing, it pales in comparison to the rates from 30 and 40 years ago.

The pandemic shifted people all over the country, leading to demographic changes at warp speed.

Buyers bidding on homes and driving up the cost of housing shows the fundamental supply-demand economy at work.

‘Organic’ supply and demand principles

The lead-up to the 2007 housing collapse saw speculation, over-extended credit and other factors that artificially inflated prices.

“What we’re having now is the complete opposite. We have a market that’s run on scarcity,” Zillow’s Bachaud said. “That’s an organic and sustainable thing that’s happening. In that sense these are completely different markets.”

Alberto’s clients in San Diego are more concerned about simply finding a house to make an offer on.

And with millennials taking over as the country’s largest group of homebuyers, there’s no indication that will slow soon.

“We’re still three to four years away from the peak first-time homebuyer age in the millennial generation,” Duncan said. “Secondly, when you look at the underwriting criteria, the risks being taken in the lending space are nothing like they were back in the 2005 to 2007 timeframe.”

“Those two things together suggest it’s more of a mismatch of supply and demand,” he added.

3 Ways to Take Advantage of the Residential Real Estate Market in 2022

Combining global Covid cases (how many variants are there now??) with rising inflation costs, and the nation’s “Great Resignation”, ringing in the New Year may have felt somewhat ‘meh’ this go around. Uncertainty in so many areas and fear of what’s next (at least the murder hornets came and went) are understandable outlooks, particularly when it comes to our personal financial stability. However, one bright spot economically that continues to shine in the U.S. is real estate. How can you take advantage of the residential real estate market in 2022 for a win?

- Buyers– If you didn’t move forward in 2021 in the purchase of your new or next home for whatever reason, now is a great time to make it happen. The unprecedented low housing inventory from last year, in both resale and new construction, remains on trend for this year but for motivated buyers with proper expectations, this will not be a hindrance.

Home prices are still rising but not as meteorically fast for resales (new construction has the disadvantage of continued labor shortages as well as supply costs). According to the Atlanta Realtor Association, 2021 saw a whopping increase of 21.6% compared to 2020 but experts are a bit more bullish for 2022 after first quarter. According to predictions, prices should start to slow down and normalize. And yes, interest rates are creeping up but they are still just around 4%, historically low, and with lower interest rates comes more buying power.

However if inflation continues to trend upwards, mortgage interest rates will probably follow suit. If you continue to delay, you may strongly regret missing out. But if you act and buy that home you’ve dreamed about this year, you will benefit from the primary wealth building method in the U.S. economy, home ownership.

- Sellers– I’m just going to copy and paste what I wrote above because it’s staggering…according to the Atlanta Realtor Association, 2021 saw a whopping increase of 21.6% compared to 2020. “Much of what drove high price growth (in 2021) will follow us into next year,” says Nicole Bachaud, an economist at Zillow. “We will expect to see prices rising at extremely high levels for the first few months of 2022 before beginning to taper off towards more normal levels.” Even with new construction competing for buyers, the seller’s market will remain extremely robust due to the fact that there just isn’t enough inventory compared to the demand.

If your home is in a somewhat desirable location and anywhere close to move in ready, the more likely you will still garner multiple offers quickly. According to Forbes, most experts say housing demand will stay strong in 2022 unless inflation continues to outrun wages at the current feverish pace, which could stall buyer appetite. Increased competition will also depend on the trajectory of the pandemic as more sellers will be willing to list their homes as daily life adjusts to the new normal.

If you wish to take advantage of homes currently being scarce coupled with a plethora of ready, willing and able buyers, now is the time to list for the greatest financial reward.

- Homeowners- If you are already taking advantage of the wealth building principles of homeownership and have lived in your home for a number of years, you may want to consider talking to a lender and refinancing to get a lower interest rate and lower your monthly payment and/or cashing out some of the equity you have built up.

Leveraging your home value to work for you is one of the primary benefits of being a homeowner. Perhaps 2022 is the year you add the pool or finish the basement you have always wanted, or use the money as a down payment on an investment property to start building your real estate portfolio.

My hope is that if the time is right, you can make one of the above options in real estate work for you in a big way! If you need help with buying or selling, it would be our privilege to earn your business. Or if you are looking for a qualified lender or contractor to make your home improvements a reality, check out our preferred vendor tab on our website at www.themeridianway.com.

May 2022 be a year of increase and prosperity for you and your loved ones.

By Holly A. Morris, Realtor

The Meridian Real Estate Group

For Additional Blog Content, Click Here!

Curating A Welcoming Mudroom

Taking in all the considerations of family schedules and activities as well as style and function of the home, Tish Mills talks you through ways to curate a welcoming, well-utilized and beautiful mudroom for your house.

What makes a good mudroom?

Just because a mudroom is a more utilitarian space, doesn’t mean it has to be utilitarian. A good mudroom space should have all the functionality that you would expect, but also all the beauty comparable to a great main entrance.

What do you need to consider when creating a mudroom?

First, I start with the basics, such as how many kids does the family have? Any pets? What are the family’s activities and needs around school? Also, what are the surrounding areas? Georgia red clay? Rainy part of the country? Once I’ve gotten the needs and wants, then I can think about the spaces nearby and how they will function together, taking into consideration how it will become an extension of the main living areas. Then the true mudroom design begins.

Are there some materials you prefer over others for flooring?

Stone is my preference for the easy clean up. The stone in the picture attached happens to be porcelain, which is even easier and no need to seal when installing.

What do you suggest to organize the space?

Storage, storage, storage. I do plenty of the locker set-ups. When I do these, I consider the ages of the kids and will plan for the future from there. But that’s not the only solution. I also like storage solutions that completely close up, like the image attached or a built-in dog crate which at times, like in my own house, can be the perfect solution.

As these are also considered entries, how can you make them stylish?

In the South, these mudrooms are typically called the “Friend’s Entrance” since they are typically right off the driveway or garage. I conceal as much of the storage as possible and add an interesting piece of furniture. Good, interesting lighting is a must.

How do you blend indoors with outdoors as this is first entry point?

I typically blend the spaces through the flooring. Then I connect the rest of the space to the main part of the house. I also love using a good, durable and stylish vinyl wallpaper for the little fingerprints that often come through a mudroom.

Tish Mills Kirk of Tish Mills Interiors, a preferred vendor of The Meridian Real Estate Group, is an award-winning interior designer who has been working with clients in their homes for more than two decades. She believes that it is essential to put together a cohesive plan for your home renovation before you get started that can be carried out by the team of experts you assemble. www.harmoniousliving.net

For Additional Blog Content, Click Here!

For more info, contact:

Beth Dempsey – Images & Details, Inc.

203.962.3235

[email protected]

Photos provided by Chris Little.

HOME TIPS TO HELP BANISH THE WINTER BLUES

Ok, who’s the genius who thought that turning our clocks back an hour, prolonging winter’s darkness even more, was such a swell idea?

Turns out, it was Benjamin Franklin, in 1784, when he proposed it in a satirical essay. According to scholars at The Franklin Institute “He merely suggested Parisians change their sleep schedules to save money on candles and lamp oil.”

Regardless of the tongue-in-cheek nature of the suggestion, the idea of “daylight-saving” was kicked around for more than a century until New Zealander George Hudson took it and ran with it.

Fitting more daylight into our days is typically welcome, but the sudden switch to darkness when we “fall back” in autumn causes trouble for some folks. Fortunately, there are some simple tricks to help us get through it.

Let Lighting Do The Heavy Lifting

Seasonal affective disorder, or SAD for short, “…is a type of depression that’s related to changes in seasons,” according to the professionals at MayoClinic.org. “Symptoms start in the fall and continue into the winter months…”

One of the treatments for SAD is a bright, light-emitting box. But you don’t have to suffer from seasonal affective disorder to benefit from increased lighting in your home this winter.

Open heavy drapes when you’re home during the daytime. Ensure windows and screens are clean to allow maximum levels of natural light to flood the home. You can also add more lamps and other lighting to the home to banish the darkness and gloom. For an added punch, increase the number of mirrors on the walls. They’ll help reflect existing light.

Bring The Outdoors In

The houseplant trend has been going on for years, and the pandemic put it on steroids. If you haven’t already joined the plant party, this winter might be a great time to give it a try.

“Indoor plants have drawn the attention of the scientific community because of their various benefits,” according to Min-sun Lee, Juyoung Lee, Bum-Jin Park, and Yoshifumi Miyazaki, authors of a study published in the Journal of Physiological Anthropology.

These benefits include:

- Stress reduction

- Improved mood

- Enhancement of cognitive health

Interaction with your plants is key to receiving these benefits, so go plant shopping, then vow to transplant, water, and generally hover over your leaf babies all winter. For an added boost in mood, add some colorful, flowering plants to your shopping cart as well.

For Additional Blog Content, Click Here!

Industrial Listings Are Not Staying on the Market for Long in Atlanta

However, traditional key indicators, including net absorption and leasing volume, may not capture the full story of the market’s performance going forward.

Net absorption is inherently limited by the amount of space tenants are able to physically occupy. Atlanta’s vacancy rate is hovering at a record low of roughly 3.5%, indicating very few vacancies exist across the metropolitan area.

Therefore, net absorption will likely track closely with net completions, at least in the near term, as prospective tenants looking to expand in Atlanta gravitate to new properties because those are essentially the only ones with suitable space available.

Because of this phenomenon, net absorption in 2022 is likely to slow compared to the more than 36 million square feet absorbed in 2021. However, that slowdown will not be due to a lack of demand, but rather a lack of available space in the market.

Of course, there are other ways to quantify and track the health of the market, such as leasing volume and rent growth.

However, when looking to quantify demand trends, it is useful to analyze how long space has been on the market before it is leased, which gives a sense of the velocity of leasing activity. This is valuable, as it is important to understand how long it may take to backfill a relet availability or to fill a new speculative facility once that space hits the market.

Median months on market tracks how long industrial space in a given geography has been marketed as available. In Atlanta, the median months on market plummeted from more than 20 months in 2014 to about six months by early 2019, and has hovered between six and eight months since then. This shows that there are few industrial listings in Atlanta that have been sitting on the market for an extended period of time, and that most of the current listings in the market have only been available for a few months.

Median months to lease is a similar metric to median months on market, but it tracks how quickly spaces are leased after they come on the market rather than looking at how long current availabilities have been on the market. For example, in the fourth quarter of 2021, the median industrial space that was leased in Atlanta had been on the market for only 4.6 months — far below the median month to lease in the early 2010s.

Both of these stats indicate that when industrial spaces come on the market in Atlanta, they are being quickly snapped up by tenants relative to the market’s historical norms.

Even if industrial net absorption slows in Atlanta in 2022, as long as the median months to lease and months on market remain at or near record lows, the region’s vacancy rate will likely remain low and owners will remain in an advantageous position to hike rents at a breakneck pace.

Demand For Houses Is Way Up. Are First-Time Buyers Driving It There?

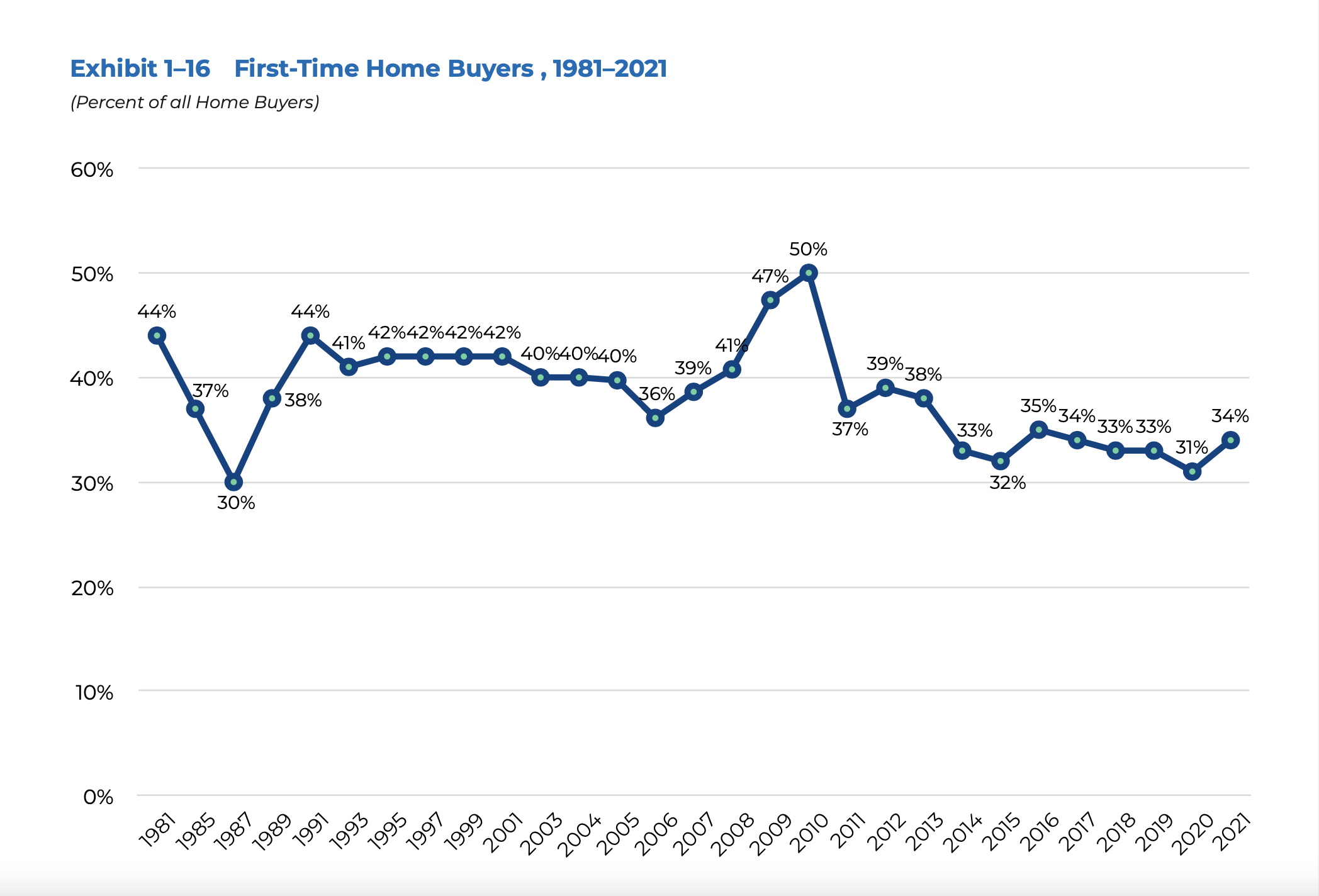

The share of first-time homebuyers was up last year, but far below the runup to the housing crash of 2008, according to NAR’s Profile of Home Buyers and Sellers. What’s happening?

The share of first-time homebuyers was up last year, but far below the runup to the housing crash of 2008, according to NAR’s Profile of Home Buyers and Sellers. What’s happening?In the immediate aftermath of the housing crash of 2008, government tax credits helped propel first-time buyers to their greatest share of home sales in at least four decades.

But when those credits expired, that share plummeted — and first-time buyers have yet to return to their typical historic levels.

Even the latest boom in housing demand has been largely driven by repeat buyers, although first-time buyers have made modest gains, according to the National Association of Realtors’ most recent Profile of Home Buyers and Sellers.

First-timers made up 34 percent of the homebuyers surveyed in 2021. That’s a three-point jump from 2020, but roughly on par with what NAR has recorded each of the previous four years.

It’s not for lack of trying. Hopeful first-time buyers may well be entering the homebuying process in greater numbers than in years past. But the same is true of repeat buyers, who come armed with more cash, more experience on the market and less exposure to risks that could set them back on the home search.

“As home prices increase, generally first-time buyers are hit hardest because they have no previous home on which to draw equity,” Jessica Lautz, NAR vice president of demographics and behavioral insights, said in a news release. “Furthermore, in the current environment, these buyers also face soaring rent prices and high student debt balances, which makes it extremely difficult to save for a down payment.”

Meanwhile, older cohorts of repeat buyers were older on average in 2021, and were in a position to carry more equity into their next home transaction as prices soared.

And as mortgage rates continue to climb from last year’s all-time lows, it’s unclear how many prospective first-time buyers have missed the boat, for now.

Treading water

It wasn’t always this hard for first-time buyers.

NAR’s survey goes back four decades. The first time the trade organization released this report in 1981, it found 44 percent of buyers were purchasing their first home.

In the years since, the share of first-time buyers has typically hovered around 40 percent. In that light, first-time buyers in 2021 were running well behind previous generations.

Today’s buyers also have a different makeup.

Repeat buyers have been aging — and growing wealthier. While the median age of a first-time buyer stayed steady last year at 33 years old, the typical repeat buyer’s age reached an all-time high of 56.

More than half of repeat buyers said they used equity from their previous home sale toward their down payment — a luxury first-time buyers simply don’t have.

Roughly 3 in 10 first-time buyers said saving for the down payment was the toughest step in the homebuying process. A significant share of first-timers said family or friends assisted with their down payment, offering gifts or loans to help them close the gap.

More than half of first-time buyers said they had to cut back on their lifestyle to prepare for the home purchase. This often came at the expense of spending on entertainment, clothing and luxury goods, NAR’s survey shows.

Still, the typical down payment from a first-time buyer was 7 percent. The typical repeat buyer was able to cover 17 percent of the purchase price in cash.

This made first-time buyers more reliant on financing than repeat buyers on a year when mortgage lenders were juggling a larger number of refinances, according to Zillow’s most recent Consumer Housing Trends Report.

“Mortgage buyers were 50% more likely to report facing at least one denial before ultimately being approved in 2021 than they were in the previous year,” the report reads.

First-time buyers were also at a disadvantage in household income. In NAR’s most recent survey, half of first-time buyers made at least $86,500 in 2020. That’s more than the typical U.S. resident, but significantly less than the typical repeat buyer. Half of repeat buyers reported making $112,500 that same year, up from $106,670 the previous year.

As home prices continued to climb and mortgage rates rose in the final months of 2021, wages across much of the country failed to keep up with housing costs, according to a report from Attom Data Solutions.

If that trend continues in the coming months, first-time buyers may find it difficult to gain ground.

Thank you www.Inman.com for this article. For more articles like this, Click Here.

For Additional Blog Content, Click Here!