U.S. MORTGAGE RATES FALL TO ALL-TIME LOWS THIS WEEK

Record lows: The average 30-year fixed rate is 2.86% this week, and the 15-year is 2.37%, Freddie Mac says

Record lows: The average 30-year fixed rate is 2.86% this week, and the 15-year is 2.37%, Freddie Mac says

Average mortgage rates for 30-year and 15-year mortgages fell to all-time lows this week, Freddie Mac said in a report on Thursday.

The 30-year average is 2.86%, breaking the prior low of 2.88% set in the first week of August, and the 15-year average is 2.37%, beating last week’s record low of 2.42%, the mortgage financier said.

The rates are driving demand in the housing market, helping to counter-balance an economic slowdown that showed signs of worsening after the COVID-19 pandemic flared in some of the nation’s largest states in recent months, said Sam Khater, Freddie Mac’s chief economist.

“These low rates have ignited robust purchase demand activity,” Khater said.

U.S. home sales surged at a record pace in June and July as purchases that were delayed during pandemic lockdowns were shifted later in the year.

Seasonally adjusted existing-home sales jumped 25% in July, beating the prior record monthly gain of 21% set in June, the National Association of Realtors said in an Aug. 21 report.

The supply of homes on the market was the lowest for any July since NAR started tracking the data about five decades ago, said Lawrence Yun, NAR’s chief economist.

Existing home sales in 2020 likely will total 5.4 million, a gain of 1.1% from last year, Yun said. Sales of new houses probably will rise 17% to 800,000, Yun said.

Early in the pandemic, before it was clear the Federal Reserve’s intervention in the bond market would drive mortgage rates to all-time lows, Yun projected home sales in 2020 would plummet 15% this year.

“The buyers are coming in because of the low interest rates – that’s the No. 1 reason in my view,” Yun said in an interview.

HousingWire.com September 10, 2020, 10:00 am By Kathleen Howley

Atlanta Industrial Market Shines As Other Sectors Are Slow To Recover

According to the latest report from the Bureau of Labor Statistics, Atlanta has added back a little more than half of the jobs lost during the initial shutdown due to the global pandemic, but the most recent jobs report shows a vast slowdown in those jobs gains during the last two months. The reports show that as Georgia became a coronavirus hot spot in July job gains slowed with the accompanying reduction of economic activity. As virus numbers are now beginning to trend down experts are hopeful that the economic recovery in Georgia will again pick up the pace.

According to the latest report from the Bureau of Labor Statistics, Atlanta has added back a little more than half of the jobs lost during the initial shutdown due to the global pandemic, but the most recent jobs report shows a vast slowdown in those jobs gains during the last two months. The reports show that as Georgia became a coronavirus hot spot in July job gains slowed with the accompanying reduction of economic activity. As virus numbers are now beginning to trend down experts are hopeful that the economic recovery in Georgia will again pick up the pace.

In another example of the pandemic’s negative economic impact, Coca-Cola announced plans to eliminate thousands of jobs in an effort to reorganize operations in reaction to less sales worldwide in the hospitality and restaurant industries.

“Given the ongoing uncertainty surrounding the coronavirus pandemic and levels of lockdown, the ultimate impact on full year 2020 results is unknown,” Coke said in its second-quarter earnings statement. “The company’s balance sheet remains strong, and the company is confident in its liquidity position as it continues to navigate through the crisis.”

The impact of the pandemic on the economic statistics has generated observable trends in the commercial real estate market in Atlanta. Amongst the four major commercial property types retail has been the most affected by the pandemic. The office market has also seen a slow down in leasing activity, but Atlanta’s industrial and multifamily markets are both amongst the leaders of the economic recovery nationwide.

Industrial

So far there has yet to be an overall negative effect to the industrial real estate in metro Atlanta from the pandemic. Leasing activity has not stalled due in large part to an industrial space leasing spree in the region from Amazon, signing four new leases in Georgia since the start of the pandemic. Amazon is not alone as other large companies have made significant commitments in the region including, Walmart, the Home Depot, and Purple.

While leasing activity remains strong there is a concern that the amount of space coming in the construction pipeline will add supply-side pressure causing vacancies to rise. However, for the immediate future it appears that the leasing volume will keep pace with increasing supply. Georgia benefits from its cheap land, multiple rail lines and interstates and the fastest growing port in the nation, the Port of Savannah.

Office

There have been many theories as to the long term effects of the pandemic upon the office market. Obviously, more people are currently working from home than at any time in recent memory, and modern technology is responsible for making that possible. This trend will almost undoubtedly have an impact on the long-term performance of the office market.

In the Atlanta metro area monthly leasing activity is down about 30 to 40% when compared to recent historical averages. Both urban and suburban areas saw a steep drop in office leasing activity immediately after the onset of the pandemic and only a slight recovery of activity since. A massive office lease was signed by Microsoft in Midtown helped to buoy urban office leasing performance in Atlanta, but take out that deal which alone accounts for 100% of Atlanta leasing for a typical month, and there is an even bleaker picture.

It appears that the slowdown in office leasing will continue for the foreseeable future, as firms nearing the end of their current lease commitments are not likely to sign long-term extensions with so much uncertainty in the business climate.

Multifamily

Despite the summertime rise of Covid cases, Atlanta’s multifamily market continues to recover at a pace higher than the other tech heavy downtown locales. While leasing activity has picked up over the last few months there are still significant challenges moving forward. Supply is peaking while job growth in the area has slowed.

The recovery within the multifamily market has varied for different locations and price points. Rents fell significantly across the board in the weeks immediately following the initial economic shutdown. In premiere urban locations, like Buckhead and Downtown, rents have remained flat with the only exception being West Midtown where rents are improving. While the more blue-collar suburban markets like Henry County and Clayton County have led the recovery.

As for the long term outlook there remains great uncertainty and performance over the next few months will depend greatly upon government stimulus and the status of the overall public health crisis. Multifamily construction activity has slowed greatly due to this uncertainty.

Retail

Atlanta’s retail sector has been significantly affected by the pandemic, as many retail locations had to either temporarily shut down or limit their services in some way. Even with Georgia being one of the first states to reopen their economy, the retail market as a whole will not return to pre-pandemic levels for quite some time. Retail vacancies are expected to continue to rise over the next few months leading to weaker rent growth and slower transaction activity.

The retail market in Atlanta was strong heading into the pandemic, but while leasing activity has increased somewhat in recent months more retail businesses and restaurants are continuing to shutter permanently. There have been significant shifts in business models in reaction to the pandemic, but it remains to be determined how long it will take for the retail market to recover in metro Atlanta.

We Can Help

Whether you’re looking to lease, buy, or sell commercial property, now is still the time to do it in Atlanta. The Meridian Real Estate Group has been assisting commercial clients for well over a decade and would love the privilege of earning your business. Our goal is not just to help our clients with a transaction, but to support the building of financial legacies through real estate. Call us today at 678-631-1723 or visit us online at www.themeridianway.com. We look forward to serving you.

For Additional Blog Content, Click Here!

The Unemployment Rate is Saving Forbearances

Forbearance housing market crash bros have a problem. Jobs are coming back faster than they thought.

Back in April, when the COVID-19 data and unemployment numbers were at their worst, the housing bubble boys had a halfway legitimate 2020 housing market crash thesis. If unemployment rates had stayed between 20%-30%, the economic damage down to homeowners would have been epic. This could have led to a rapid increase in inventory on the market, which would have crashed home prices as demand collapsed.

That didn’t happen, of course.

Instead, the U.S. housing market has been the best-performing economic sector in the world during the pandemic. This alone should make you question those ridiculous bubble boy websites, the trolling Facebook friends, and those Youtube videos of the same ilk. (Those YouTube videos are especially egregious).

It is easy to go on Facebook, Twitter, or YouTube and say the current housing market is like 2008 all over again – but if you dig just a little bit deeper into the numbers, that thesis quickly falls apart.

Before we go into the data I believe it’s time to move the Housing Bubble Boys over to their new name: the Forbearance Housing Market Crash Bros.

There is one problem the forbearance housing market crash bros have now: jobs are coming back.

Unemployment during COVID

Only during the Great Depression of the 1930s was the employment rate more heartbreakingly bleak then it is now during the COVID-19 recession. Although methods of measurement may not have been as sophisticated then as they are now, the unemployment rate was estimated to have reached as high as 25%, with 15 million Americans unemployed in 1933.

In April of 2020, the unemployment rate reached 14.7%. Currently, the total unemployment rate stands at 8.4%.

At peak unemployment in April, women 20 years and older suffered higher unemployment (15.5%) then men 20 years and older (13.0%) – and this is due to the over-representation of women in the hospitality and service sectors, the hardest hit by the crisis and stay-at-home mandates. Today we have seen improvement in both, as the unemployment rates for men over the age of 20 is 8% and women over the age of 20 is 8.4%.

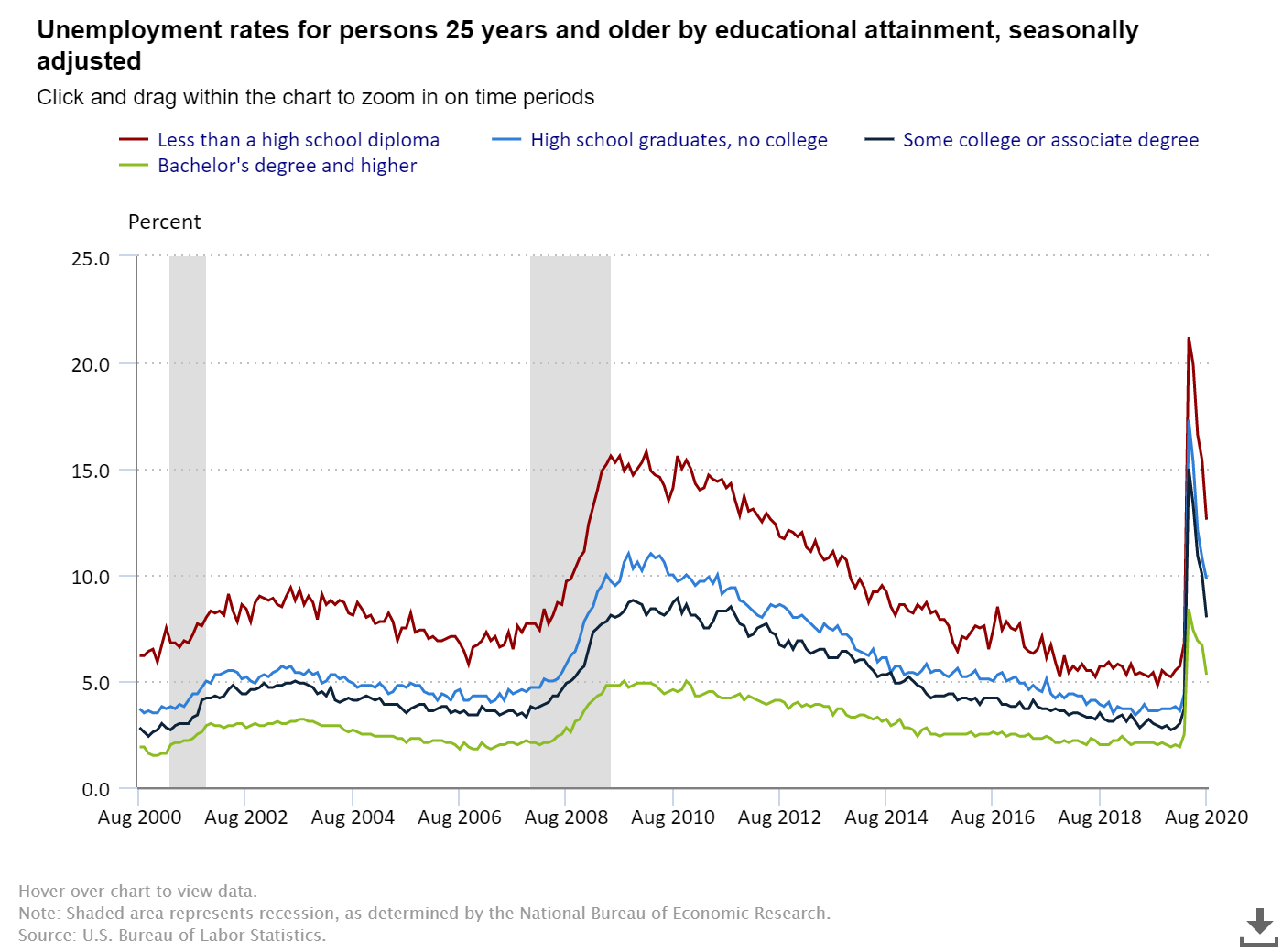

The unemployment rate has also been inversely proportional to education level. Those with more education and in higher-paid positions have been less affected by job losses. The unemployment rate among those with less than a high school diploma is 12.6%, for those with a high school diploma it is 9.8%, for those with some college or an Associate’s degree it’s 8%, and for those with a Bachelor’s degree or higher, the rate stands at 5.3%. From this, it is both intuitive and factual that the burden of job losses was shouldered more by workers with lower incomes.

Because the unemployment crisis has been significantly worse for those with lower incomes, the economic consequences, too, have been considerably worse for renters compared to homeowners. Also, fiscal and monetary disaster relief along with forbearance are factors for why we should not expect a glut of foreclosures due to the high unemployment rate.

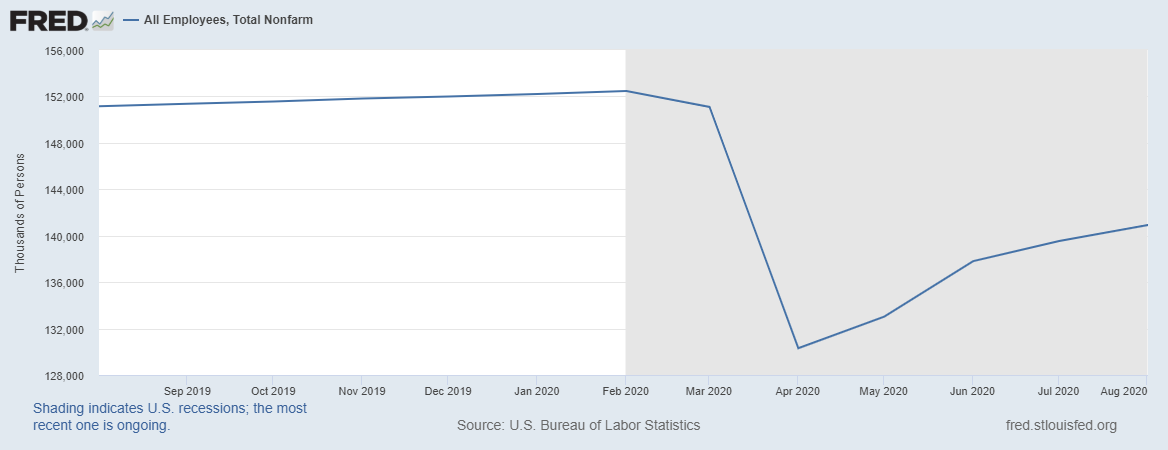

Remember, even with the high unemployment rate (which is back to single digits); we will have over 140 million Americans working and the existing home sales market needs 4 million new mortgage buyers a year to be stable.

Forbearance

To be sure, homeowners with mortgages did suffer job losses due to COVID-19. But we are still early in the job recovery process. As more Americans return to work, they are more likely to get off forbearance plans, though this may lag job gains by a few months. As long as job growth is positive and the U.S. government continues to financially and monetarily support the economy with disaster relief, it is doubtful the housing market will crash in 2021, even if the forbearance plans end, which is still a questionable outcome. Whoever wins the presidential race in 2020 might not want to see the forbearance plans expire if we are still far below the peak job numbers we had in February of 2020.

Since the peak, roughly 10.6 million jobs have been recovered. A healthy proportion of these job gains have been due to rehires for jobs that were lost, rather than newly created jobs – so this is the easier portion of the recovered employment. The more challenging work for the country is the creation of new jobs after we recover the remaining 11.5 million jobs needed to get back to the employment levels of February of 2020. Some of the jobs lost are not coming back so easily, as permanent job losses have increased to 3.4 million.

While we have had four months of job gains, the rate of growth is slowing. It’s impossible to have the U.S. economy and the world economies run as they did before COVID-19 while the virus is still active. Certain industries will be at a disadvantage versus the virus for many months to come while others do benefit from this crisis.

Sooner than later, we will earn the right to have more labor in the marketplace. Once the virus is under control of an effective vaccine, more labor will be needed as people can walk the earth freely again.

However, the most critical point I want to make here is that one of the biggest factors for the housing market crash thesis in 2020 was high unemployment and that is starting to fade. I urge my forbearance crash bros to be patient and wait until December of 2020. Then I can give you an actual model on how likely your 30%, 40%, or 50% home-price crash thesis for 2021 will be.

HousingWire.com September 8, 2020, 12:02 pm By Logan Mohtashami

For Additional Blog Content, Click Here!

Lumber Prices to Skyrocket More Than 160%

The COVID-19 pandemic has caused lumber prices to skyrocket more than 160% since April after a spike in home renovation by cooped-up Americans, according to the National Association of Home Builders.

The COVID-19 pandemic has caused lumber prices to skyrocket more than 160% since April after a spike in home renovation by cooped-up Americans, according to the National Association of Home Builders.“As people started nesting in response to the pandemic, they started undertaking all sorts of home renovation projects,” Dietz said. “At the same time, sawmills started shutting down and have only partially reopened because of social distancing concerns.”

The lumber industry lost 6,000 jobs as a result of the pandemic, and has gained back – on a net basis – only half of those, he said.

“Growing demand for lumber met insufficient supply, and the result has been escalating prices,” Dietz said.

The above excerpts were taken from an article titled Spike in lumber prices boosts construction costs, written on September 4th, 2020 by Kathleen Howley for HousingWire.com

For Additional Blog Content, Click Here!

Know Your Neighborhood: Marietta

Now known for its bustling city square, Marietta was once home to Creek and Cherokee Indians. The birth of Marietta began with 4 community homes near an old Indian Trail which accounted for less than 50 people. The city was named after the wife of T. R. R. Cobb, Mary Cobb. Hence the county of which Marietta lies in, Cobb County. Marietta was formally established into a county seat in 1834.

Now known for its bustling city square, Marietta was once home to Creek and Cherokee Indians. The birth of Marietta began with 4 community homes near an old Indian Trail which accounted for less than 50 people. The city was named after the wife of T. R. R. Cobb, Mary Cobb. Hence the county of which Marietta lies in, Cobb County. Marietta was formally established into a county seat in 1834.

In 1837, Marietta was chosen as a home base for the Western and Atlantic Railroad running from the Chattahoochee to the Tennessee River. The railroad was finally completed in 1842 which resulted in Marietta emerging as a popular stop. Surrounded by Kennesaw Mountain and Little Kennesaw Mountain, Marietta became quite the tourist destination.

Marietta also played an important role in the Civil War. Union soldier, William Sherman took control of the city and the surrounding Kennesaw Mountain from the Confederate Army July 2-November 14, 1864. The Fletcher House, later known as the Kennesaw House, became an important base for many important Union soldiers. Atlanta was finally captured by the Union Army which led to the South surrendering in April of 1865 and reconstruction of the city began.

Marietta served as home base for the Bell Bomber factory during World War II which was based at Marietta’s Rickenbacher Field. The Bell Bomber factory built 669 B-29 bombers used by American forces during the war. After being abandoned in 1951, Charmichael and Lockhead Corporation rescued the plant, which lead to the birth of Lockeed-Martin. Lockheed-Martin is one of the major employers of the state.

The next time you are in Cobb County, make sure you stop by the hip city square that offers a beautiful center with a fountain and small stage for summertime entertainment. During Spring and Summer weekends, the square offers art walks, a concert series with live entertainment, The Taste of Marietta and many more fun events to attend. The square is surrounded by an array of restaurants with outdoor seating as well as Glover Park Brewery and soon to be open Red Hare Brewery at the old Hemingway’s location.

By our Preferred Vendors, Neel Robinson & Stafford, LLC, on September 8th, 2020

For Additional Blog Content, Click Here!

A Strong Warning from Professional Realtors Why Now May NOT Be the Time to Buy a Home

Professional Realtors take their fiduciary responsibility to clients quite seriously and although seemingly counterintuitive, may strongly advise AGAINST buying or selling a home right now if certain criteria apply. This month The Meridian Real Estate Group will explore the TOP 5 reasons NOT to buy a home in today’s market.

Do NOT buy if:

1) You prefer to keep up with the Joneses- This is understandable. Most of your friends and family have mortgage interest rates that average between 5.25% all the way up to 9%. You may not want to surpass your peers by taking advantage of current historically low interest rates that start in the low 3’s (not a typo). Imagine the stares and subsequent deferential treatment at parties and other social gatherings this would garner when others realize how much more financially savvy and sophisticated you are. This could be quite unnerving if you’re not used to winning in life.

2) You prefer less cleaning and yard maintenance- After all, who wants more square footage or land to take care of? By leveraging the lower interest rates in your favor, you may accidentally stumble into a much larger home and/or lot you would not have been able to afford otherwise. It’s basic math…more square footage and acreage equals more dusting, sweeping, gardening, etc. Super boring. Instead you could be bingeing the latest streaming show with a giant bag of barbeque chips in your lap and a box of powdered doughnuts as back up. The only thing you would need to worry about dusting off in this scenario would be your clothes and couch. All. Day. Long.

3) You don’t like people in your personal space- This goes hand in hand with the basic math mentioned earlier. If you prefer solitude over socializing, don’t buy now or you may get more home for your money. You could gain another bedroom or worse yet an in law suite and then what? Random friends and family just assume they can not only visit but stay for awhile?? Your cats would be traumatized. Nope, nope and nope. Wisely keep your socialization in public places, not private spaces.

4) You prefer above ground storage- Many Americans these days have handily converted their garages into large storage spaces and are parking their cars in the driveways, thus giving them more access to the elements such as sunshine, rain and bird droppings. Although this may be detrimental to the paint job and interiors of said automobiles, this probably makes the cars happier and definitely employs multiple car washes in the area. Plus as your garage inevitably fills up over time, you will have the added benefit of periodically becoming a local garage sale guru. We recommend not buying a home with a basement (which you may be able to afford now with the ridiculously low interest rates) if waking up at 5:30am to haggle with professional garage sale shoppers over a dented colander thrills you in any way.

5) You are a natural DIYer- There are so many advantages if you are a type A creative personality to stay where you are. With affordability to better locations possible with the low, low, low interest rates currently, avoid the temptation to move to a better area that may be closer to conveniences such as shopping, top rated schools or access to highways. Instead, jump on the world wide web and learn how to DIY just about anything! Uh oh, you ran out of butter? Learn how to churn your own from expired milk. Farther away from the school district you would like little Johnny in? Simply become a homeschooling superhero via online courses and spend every waking hour together. You barely see your significant other because it takes them hours to drive to and from work? Become sufficient at different languages and/or accents and you can entertain yourself endlessly with stimulating conversation by tricking your mind into believing someone else is there. The possibilities are endless.

This list is far from comprehensive but gives a good foundation in determining whether or not you may fall into the category of someone who would NOT benefit from buying in today’s market with the ridiculously low interest rates. Next month we will cover why now is NOT the right time to SELL your home. Until then, if you do decide to buy or sell real estate, give us a call. We would love to help.

By Holly A. Morris, Realtor

For Additional Blog Content, Click Here!

Atlanta’s Commercial Real Estate Market Outpaces Other US Metros Since Pandemic

The United States added 7.5 million jobs in May and June, which is about a third of the jobs that were lost in the previous 3 months during the initial phase of the global pandemic breakout and shutdown. Atlanta and the rest of the sunbelt metro areas outside of California have performed well in relation to the overall national job numbers. However, a rise in cases in Texas and Georgia threatens to dampen the overall optimism of quick v-shaped recovery across the South.

The United States added 7.5 million jobs in May and June, which is about a third of the jobs that were lost in the previous 3 months during the initial phase of the global pandemic breakout and shutdown. Atlanta and the rest of the sunbelt metro areas outside of California have performed well in relation to the overall national job numbers. However, a rise in cases in Texas and Georgia threatens to dampen the overall optimism of quick v-shaped recovery across the South.

New York posted some of the strongest job gains in June. Orlando, on the other hand, with its reliance on a tourism economy, continues to lag behind the rest of the nation. Metro Atlanta initially lost approximately 300,000 jobs from March to April but has since added back roughly half of those jobs. The next few jobs reports should more clearly indicate the effect of the recent rise in case of numbers in Georgia upon the overall economic recovery of the state.

The rise in cases has done little to stop Atlanta’s industrial market as it is currently a leader nationwide. The multifamily market in the metro area remains strong compared to other locales, while the office and retail markets remain in precarious economic positions. Here is a closer look at each of these sectors of the Atlanta commercial real estate market.

Industrial

Given the circumstances of the economic situation as a whole, Atlanta’s industrial market continues to show its muscle. With a recent flurry of activity Atlanta now ranks second nationally in the amount of industrial space currently under construction at nearly 25 million square feet, trailing only the Dallas-Fort Worth metroplex. Current leasing velocity has helped to silence the concerns of adding too much inventory to the market as almost half of the space under construction is already preleased.

Growing firms are targeting areas south of I-20 for industrial space. The southside of Atlanta should continue to see new industrial construction and move-ins due to its relatively unclogged roads, favorable zoning, and strategic location near the airport and the Port of Savannah.

Home Depot announced plans to open three new distribution centers in Georgia as part of a larger nationwide initiative to upgrade its supply chain to better meet the growing demand of online shopping. The new Georgia facilities will be located in DeKalb, Fulton and Henry counties in the Atlanta metropolitan area.

CoStar managing analyst David Kahn commented on Home Depot’s plans as part of a larger national trend for retailers. “The importance of same-day and next-day delivery continues to drive decisions by major distributors throughout the country, and we’ve seen companies such as Home Depot expand to new, highly-efficient facilities throughout the country in order to better service their brick and mortar footprints,” Kahn said. “While e-commerce and same-day and next-day delivery is often focused on business-to-consumer operations, for Home Depot in particular, this is important for their business-to-business operations, too.”

Multifamily

Atlanta’s multifamily recovery is among the leaders of cities across the nation. Atlanta rents fell during the early months of the pandemic but have come surging back as of late. Atlanta joins Portland and Philadelphia as the only three major US cities whose rents are above pre-coronavirus levels. Although this appears to be a positive trend in comparison to the rest of the country, it is still close to nil in rent growth for year over year marks, having missed on the usual surge in springtime demand for apartments.

There is growing concern that the rapid rent recovery is not a sustainable trend amongst the recent rise in case levels in Georgia and as temporary jobs losses increasingly appear to be long-term in nature. Continued rent growth will undoubtedly be tied to the effectiveness of the government’s public health response and economic recovery stimulus packages, specifically regarding enhanced unemployment benefits.

Another trend worth noting since the pandemic hit is that renters in the Atlanta area have seemingly shifted the demand towards more affordable suburban locations. Cherokee County, Clayton County, Southeast DeKalb, Westside Atlanta and South Fulton have shown the strongest gains in 2020. These areas have ample mid-tier apartments available and lower asking rents in comparison with their urban Atlanta counterparts. Buckhead and Midtown have struggled to add new renters since the pandemic hit.

Office

Before the pandemic hit, Atlanta’s office market had enjoyed years of increased rent growth and high occupancy rates. While the city has recently secured large commitments for office space from companies like Microsoft and Google, the weakness in this sector is beginning to show. One key indicator, space available for sublease, has steadily increased during the first half of the year. This would typically signify a future softening of the office market in the near term.

As an example of this trend, Buckhead has seen large amounts of sublet space go on the market recently. Areas with a higher concentration of sublet space will be especially vulnerable to a prolonged economic downturn as coronavirus cases rise and the pandemic grinds on into the fall and winter months.

Developers remain optimistic about Atlanta’s long term office outlook, and while there will undoubtedly be short term pain in the market, the metro area’s highly educated workforce, lower rents, and relatively affordable cost of living should continue to attract new office tenants.

Retail

Leasing activity for retail in metro Atlanta has slowed to minimal pace following the national trend as retail and hospitality have been the hardest hit sectors of the commercial real estate world. The pandemic has caused a massive shift towards online shopping and food delivery services and brick mortar retailers are struggling to adjust and fighting to survive.

Retailers nationwide have backed out of preplanned expansions and are hesitant to commit to renewals. The second quarter of 2020 was one of the worst in recent history in terms of retail leasing in metro Atlanta. Net absorption was negative for the first time in almost a decade. It remains to be seen how long this downturn will last and what the retail recovery will look like, but one thing is for certain – it will not be the same as before the pandemic hit for a long time, if ever.

We Can Help

Whether you’re looking to lease, buy, or sell commercial property, now is still the time to do it in Atlanta. The Meridian Real Estate Group has been assisting commercial clients for well over a decade and would love the privilege of earning your business. Our goal is not just to help our clients with a transaction, but to support the building of financial legacies through real estate. Call us today at 678-631-1723 or visit us online at www.themeridianway.com. We look forward to serving you.

For Additional Blog Content, Click Here!

Can Adaptive Reuse Save American Malls?

What is the most common reason to get in the car and start driving on any given day of the week? Depending on where you’re from, the obvious answer might be commuting to work. Surprisingly, though, this is not the case. According to the Department of Transportation as of 2017, 41 percent of daily trips are for shopping and errands, 27 percent are for social or recreational travel, and fifteen percent are for commuting. Retail is not only the biggest category of trips by volume, but it also represents a hugely oversupplied property use in the U.S. according to data from the International Council of Shopping Centers and Cushman & Wakefield: 23.5 square feet per person, as opposed to the next highest, Canada, with 16.8 square feet per person. After Australia, at 11.2 square feet, no other surveyed country exceeded 4.6 square feet per person.

What is the most common reason to get in the car and start driving on any given day of the week? Depending on where you’re from, the obvious answer might be commuting to work. Surprisingly, though, this is not the case. According to the Department of Transportation as of 2017, 41 percent of daily trips are for shopping and errands, 27 percent are for social or recreational travel, and fifteen percent are for commuting. Retail is not only the biggest category of trips by volume, but it also represents a hugely oversupplied property use in the U.S. according to data from the International Council of Shopping Centers and Cushman & Wakefield: 23.5 square feet per person, as opposed to the next highest, Canada, with 16.8 square feet per person. After Australia, at 11.2 square feet, no other surveyed country exceeded 4.6 square feet per person.

In our newest research report, we explore the logic and risks beyond repurposing properties whose uses have become obsolete. But an interesting scenario appears when the property in question is not totally obsolete. Are there opportunities to eat up some of that excess retail space by combining multiple property uses within the shells of existing, somewhat but not totally obsolete properties? Consider a shopping mall facing growing vacancies. Around two hundred and fifty J.C. Penney stores may be closing, along with other familiar mall anchor and non-anchor tenants like Neiman Marcus and Victoria’s Secret. Instead of trying to re-tenant these spaces with other retail occupiers, mall owners could hang on to their well-performing, smaller tenants and redevelop some of the extra space into apartments.

Such an approach would suck up a lot of square footage quickly, while also providing the remaining mall tenants with a built-in captive audience. No matter where you live, picture your nearest shopping mall. Now imagine you live on-site. How often would you leave the property premises to shop somewhere else? Even if your shopping excursion requires a car, it would be easier and quicker to take a three-minute trip through the parking lot than a ten-minute drive down the highway.

Building residential space into malls offers other advantages, too. Grocery stores could deliver bags of food to runners employed directly by the landlord who could, in turn, bring everything directly into residents’ units. These blended centers could be particularly attractive to older adults, who would benefit from both the proximity to shopping and services as well as the sense of activity that being near a buzzing destination provides. And according to Steve Henenfeld, a retail broker and current executive managing director at Colliers, “Malls are typically located on or near an intersection of a highway or the main street and are well served by public transportation. That puts the residential properties at the center of town, allowing residents easy access to main roads and highway systems.”

Some might think that living in a mall is particularly nightmarish, but well-executed projects could look much like normal mixed-use developments, or manifest as separate residential towers surrounded by well-manicured landscaping, and not just like small apartments crammed into vacant big-box shells. Projects that add residential space to malls are already underway. In a northern suburb of Seattle, Alderwood Mall is developing 300 apartments that will complement the remaining 90,000 square feet of retail space at the property. Alderwood is the product of a collaboration between Brookfield and AvalonBay, titans in retail and multifamily, respectively.

No modern conversation about retail real estate could be complete without mention of the coronavirus. Adding residential space to malls would allow entire populations of people to shop at their on-site stores without having to take public transit or risk infecting another area if they are themselves infected. If things get even worse, it would be possible for on-site retail to close their doors to outsiders, cutting down transmission chances even more.

Bringing people closer to retail is only one solution for the glut of distressed malls across the country. Another solution is to add office space to malls, which similarly cuts down on commuting time since access to shopping would be available immediately after leaving the workplace. Co-working has been a noted supplement at some malls, like those of the large owner Macerich, which partnered with co-working operator Industrious last year. Traditional office space can be a potent, long-term stabilizer for shopping centers, too.

A glitzier solution than adding offices is the transition of mall spaces into entertainment venues. New malls are being built with these uses in mind. Consider the American Dream mall in New Jersey, which has both a ski hill and a water park. For property repurposes, empty anchor stores can provide useful canvases to fill with go-kart tracks, mini-golf venues, and other uses that cannot be replicated digitally at home. Amidst the coronavirus outbreak, some malls are using their parking lots as venues for drive-in theaters, allowing visitors a social distancing-friendly recreation experience.

One other possible addition to malls is distribution space. “With distribution, as long as more and more people are looking to have stuff delivered at home, the demand for space to store goods close to people increases,” said Pauline Hale, Senior Manager for Altus Group. Amazon has taken this approach, building distribution space into malls in places like Ohio.

According to Eli Finkelshteyn, the CEO and co-founder of eCommerce tool Constructor.io, “As Walmart races to catch up to Amazon technologically, Amazon is racing to catch up to Walmart in brick and mortar logistical know-how, as well as physical locations it can use as fulfillment centers for its recent one-day shipping promises. Currently, Walmart is pressing its physical presence advantages and new e-commerce abilities with programs like curbside pick-up, and Amazon knows it needs to gobble up physical locations quickly to catch up.”

Each of these solutions requires its own economic indicators to properly underwrite. Some markets will be well-supplied with housing but undersupplied with logistics space, or vice versa, and it is up to the project developer to understand exactly what is needed in a given market. It’s also up to the developer to acknowledge when a given project would push them too far out of their comfort zone, and when a partnership, as at Macerich or Brookfield, is necessary.

Each of these types of adaptations addresses the oversupply of retail space in the U.S. by combining existing, sustainable retail with other property uses. Whether office, distribution, entertainment, or residential, there are favorable economies of scale to be leveraged by this sort of project mixing. This kind of work could change the fabric of neighborhoods used to viewing the mall as just a place to shop, but it might be just what communities need to keep travel times low, delivery times short, and social distancing high.

By Logan Nagel for Propmodo Research July 15th, 2020

For Additional Blog Content, Click Here!

Atlanta’s Industrial Market Remains Strong While Other Sectors Adapt To Overcome New Obstacles

Atlanta has quickly established itself as the tech hub of the Southeast with companies like Google, Microsoft, and Amazon planning to add many more jobs in the near future. The addition of these high-paying jobs from tech firms will continue to fuel demand for office space and high-end apartments.

Atlanta has quickly established itself as the tech hub of the Southeast with companies like Google, Microsoft, and Amazon planning to add many more jobs in the near future. The addition of these high-paying jobs from tech firms will continue to fuel demand for office space and high-end apartments.

While the long term outlook remains bullish the realities of the current situation can at best be described as uncertain. Atlanta lost approximately 300,000 jobs from March to April during the initial shutdown due to the global pandemic, erasing over 4 years worth of employment gains in the city. Labor statistics are starting to show a feeble recovery as the city added 35,000 jobs from April to May, but a recent rise in coronavirus cases after Gov. Kemp’s aggressive reopening and massive protests in the streets threaten to stall the optimism of a quick, v-shaped recovery for the metro area.

Kemp is moving forward with his strategy to stem the negative tide of a prolonged economic downturn, most recently by reopening the state’s film, television and entertainment industry to continue productions. Kemp stated that film production companies are planning to invest over $2 billion into the Georgia economy over the next year and a half.

“The entertainment production industry is coming back and ready to jump-start the Georgia economy by creating jobs and generating greatly needed investment and spending in communities across the Peach State,” Kemp said in a press release.

Georgia House of Representatives Speaker David Ralston commented further saying, “The creative arts and entertainment — particularly television and film — have long been driving forces in our economy, and they will be instrumental as we recover from the impact of the pandemic. Working together, we will keep Georgia the leading destination for film and television production — thousands of Georgia jobs depend on it.”

The other big piece of real estate related news for the city is that WarnerMedia plans to sell and lease back the iconic CNN Center in downtown Atlanta. The building, with its large red CNN logo outside, was a national focal point during the recent protests sparked by the death of George Floyd, and sustained extensive damage once the protests turned to looting and rioting. WarnerMedia released a statement saying that with the five-year leaseback plan, “There will be no immediate impact to employees working at the CNN Center.”

Now let’s take a closer look at how the commercial real estate market has fared in metro-Atlanta over the last month.

Retail

The retail market has been hit hard in general by the Covid-19 shutdown but retail investment sales broker KB Yabuku with Ackerman & Co. is hopeful we are seeing the first signs of a comeback.

“For a couple of months, it was pretty quiet,” Yabuku said. “But in the past few weeks, guys have been starting to come from under the rocks. We’re definitely starting to see more activity.”

Part of that activity includes Avalon, the $1 billion mixed-use development in Alpharetta, securing four new retailers with High Country Outfitters, Onward Reserve, Restore Hyper Wellness + Cryotherapy and Tempur-Pedic deciding to open stores there. High Country Outfitters has already opened and the others expect to open by fall.

CoStar market analyst Trenton Turner stated, “Avalon sits adjacent to some of metro Atlanta’s wealthiest households and several fast growing neighborhoods. As such, retail tenants stand to benefit from high-paying consumers living and working in the surrounding communities. With a scarce amount of available retail space in urban nodes of North Fulton, Avalon will likely remain an attractive option for retailers.”

Industrial

With brick and mortar retail struggling to overcome a new reality, Internet shopping and food delivery apps have quickly expanded to fill the need of the flow of goods from producers to consumers. Atlanta has continued to see large investments from e-commerce giants like Amazon.

The company has targeted Atlanta as the hub of its Southeastern US operations, and leases about 12 million square feet of industrial space in the Atlanta region. 2020 has been a busy year for Amazon around Atlanta adding about 4.25 million square feet of distribution and warehouse space in the area with the signing of 4 new leases.

So far the pandemic has not created a slowdown in industrial leasing in the metro area. Leasing velocity has actually accelerated over the last few months. Atlanta hosts a diverse number of multinational companies that use the hub to distribute regionally and nationally. The city’s infrastructure and educated workforce will continue to make it a premier industrial hub.

Multifamily

As many people have switched from going into the office to working from home many experts expect to see a long term effect on the multifamily market. John Affleck, CoStar’s vice president of market analytics states that, “Working from home has made proximity to the office or transit irrelevant, at least for now. These realities have upended the demand patterns that have driven the multifamily market over the past decade.”

Demand for multifamily units has slowed in central business districts but has started to increase in the suburbs. “The quarter began with rents in freefall, just as the spring leasing season kicked off,” Affleck said. “Suburban product offering more space at a lower cost appears to be in high demand.”

Midtown Atlanta had recently been a fast-growing favorite of multifamily developers with a boom in multifamily construction from 2017 to 2019. Currently there are only two projects underway as developers have put the brakes on new projects to allow completed high-rises to lease up. Rent growth has not recovered in Midtown mostly due to the pandemic, but developers are beginning to respond to recent announcements of future new jobs from companies like Microsoft and Facebook with several upcoming development projects on the horizon.

The real test for Atlanta multifamily leasing comes over the next few months, during what would normally be the prime leasing season. The reopening of the Georgia economy has brought with it a recent spike in coronavirus cases. If this trend continues and if Atlanta faces a longer and more cautious reopening timeline then leasing activity in the city could remain weak for a number of months to come. This possibility would certainly slow down investment in new multifamily projects as well.

Office

It is unlikely that we are seeing the demise of the corporate office building in its entirety, but the office market will certainly be significantly impacted by a long term shift to the possibilities of working from home now that the response to the virus has shown that it can be done on a large scale basis. Owner’s of office properties will need to become more active in their tenant relationships as many companies will reassess their need for offices for a large majority of their workforce and reconfigure their office environment to account for new social distancing protocols.

Matt Bronfman, CEO of real estate investment firm Jamestown confirms the need for a more active tenant relationship saying, “The owners with the biggest struggles will be those that bought properties thinking they were just going to sit back and let the rent checks roll in, occasionally hiring a broker to fill vacant space. Successful owners are going to be those that actively partner with and support their tenants, helping both keep them in business and get them to the point where they can thrive.”

Developer Egbert Perry, CEO of The Integral Group states that, “People across many industries have had to rethink the balance between the use of technology vs. in-person engagement, and as a result, I think we are going to see some work habits change. There could be increased focus on designing residential space to have the flexibility to also serve, in part, as an office, with a technology-enabled environment to support that.”

Owners and operators of existing office buildings will need to reconsider many aspects of their office environments as currently configured. Once common solutions such as elevators and open floor plans may no longer serve the needs of office workers as many are now seeking private offices and touchless technologies and scrutinizing the cleanliness of HVAC filtration systems.

Short Term Prognosis

Although facing an unprecedented crisis of public health and civil unrest, Atlanta, with its structural advantages, will likely continue to grow at a faster pace than many other metro areas across the United States. Atlanta is home to one of the busiest airports in the world and is a hub of interstate highways and rail lines in the South. The metro area boasts a very desirable mixture for businesses of both affordability and a highly educated workforce.

Atlanta has quickly established itself as the tech hub of the Southeast with companies like Google, Microsoft, and Amazon planning to add many more jobs in the near future. The addition of these high-paying jobs from tech firms will continue to fuel demand for office space and high-end apartments.

We Can Help

Whether you’re looking to lease, buy or sell commercial property, now is still the time to do it in Atlanta. The Meridian Real Estate Group has been assisting commercial clients for well over a decade and would love the privilege of earning your business. Our goal is not just to help our clients with a transaction, but to support the building of financial legacies through real estate. Call us today at 678-631-1723 or visit us online at www.themeridianway.com. We look forward to serving you.

For Additional Blog Content, Click Here!

Americans Leave Large Cities for Suburban Areas and Rural Towns

A combination of the coronavirus pandemic, economic uncertainty, and social unrest is prompting waves of Americans to move from large cities and permanently relocate to more sparsely populated areas. The trend has been accelerated by technology and shifting attitudes that make it easier than ever to work remotely. Residents of all ages and incomes are moving in record numbers to suburban areas and small towns.

A combination of the coronavirus pandemic, economic uncertainty, and social unrest is prompting waves of Americans to move from large cities and permanently relocate to more sparsely populated areas. The trend has been accelerated by technology and shifting attitudes that make it easier than ever to work remotely. Residents of all ages and incomes are moving in record numbers to suburban areas and small towns.

A perfect storm of factors makes the decision to leave major cities like New York very obvious. The dense nature of urban living and the lack of proper local government planning led to the coronavirus spreading five times faster in New York than the rest of the country. The city that never sleeps now resembles a ghost town in many areas after thousands of its wealthy and middle-class residents fled early in the pandemic.

Many are moving to small towns north of the five boroughs. Four upstate counties have seen an incredible surge in real estate demand, while the rest of the New York market is cratering. In Ulster County, the number of homes now under contract nearly doubles the 2016 figures. It saw steady sales in March and April while the overall New York market fell by nearly 30 percent. Some people are staying at their vacation homes, but the data suggest there are many permanent moves in the works.

An estimated quarter of a million New York residents will move upstate for good, while another 2 million could permanently move out of the state. More than 16,000 New York residents have already relocated to suburban Connecticut. The preliminary figures show New York is also losing citizens to rural New England and Florida in significant numbers. Similar trends are happening in other large urban areas. There is a political element within the domestic migration at play across the nation, but what is more telling is the level of movement to suburban areas and rural towns.

Over 40 percent of urbanites have browsed online for real estate, more than twice the level of people who live in the country. Redfin reports that more than a quarter of searches on its website are by urbanites in Seattle, San Francisco, and the District of Columbia searching for homes across less populated places. While real estate sales are down in San Francisco, where prices are falling by more than 50 percent, demand in its suburbs has been soaring, where prices are rising by almost 10 percent.

There has been a sharp uptick in interest in moving out to Montana, with the majority of new inquiries coming from California. Real estate sales in Montana are 10 percent higher than at this time last year. Rural Colorado, Oregon, and Maine have seen similar upticks in property sales. Vermont is going through a renaissance in real estate, with an agent there remarking that “people are buying houses without even seeing them.”

Some of the biggest changes are less obvious, yet even the hidden trends support the idea that cities are emptying out. In March and April, over 2 million young people moved back in with their parents or grandparents. If the allure of cities declines further due to the risk of disease, a sputtering economy, and a future of telework, the flight to suburban and rural safety will continue well after a coronavirus vaccine hits the market.

Social unrest and urban crime rate spikes also raise the possibility of a sharp increase of exits from large cities. A breakdown in order, especially if police are defunded, could further downsize cities rebuilt with law and order approaches. Urban trends of the last 50 years are being reversed. Instead of smaller towns and rural areas facing the steep declines, large metropolitan areas may soon be the places bleeding citizens.

The moves and the circumstances that precipitated them will likely cause profound changes in the places receiving the most coronavirus refugees. It is still too early to forecast the political impacts of these demographic trends, but they could be significant. Floods of former urbanites could bring more taxes, restrictions, and regulations to these areas.

On the other hand, an influx of money could reinvigorate former industrial towns. A curious question is whether the waves of new residents will see these smaller areas as their real homes or as places of convenience that need to be reshaped in the image of the cities they fled from.

By Kristin Tate for ‘The Hill’ on July 5, 2020

Thank you, Redfin for this article. For the whole article, Click Here.

For Additional Blog Content, Click Here!

Home Improvements To Gain Highest Return on Investments (ROI) and Faster Sales

The Atlanta real estate market remains robust compared to the majority of other major cities in the country due to the fact Realtors were deemed essential in Georgia and pivoted quickly to facilitate safety in the showing and closings of homes during Covid-19. The amount of homes available still remains somewhat tight which is good news for sellers as more buyers are compete for less inventory. In a seller’s market, you still need to compare to other homes in your area and price range favorably. Independent of location, there are 3 primary driving factors in selling your home in a timely manner…price, condition and marketing. A good Realtor will help you determine a fair price based on a professional market analysis of comparables, as well as provide you with the marketing resources crucial in exposing your home to as wide an audience of ready, willing and able buyers as possible. The job of the home seller is to ensure the condition is as good or better than the surrounding competition in order to sell quickly at the highest price. If you have loved your home well, this may sound somewhat intimidating as to what investment this may entail, but the more move-in ready a home appears, the more readily others can see themselves in it. Returns on your investment will vary from making more money on the sale, to selling your home faster thus having less mortgage and utility payments.

-

Curb appeal- The importance of your first impression is similar to a job interview. What is the initial opinion of the decision maker? If the front of your home presents well, the buyer will immediately be excited to see more. You can do this by sprucing up your landscape by making sure weeds are pulled and your lawn is mowed. Consider adding fresh pine straw, flower beds or potted plants near the front. Repainting your front door will make it pop, and if these are cracked or outdated, replace the door handle and doorbell cover. Another easy repair is pressure washing the driveway and sidewalk. Pressure washers can be rented at home supply stores inexpensively. Any amount of money you spend from where the car is parked to the front door will typically give you a 103% return on investment.

-

Paint the interior- Unless your home is already a neutral color throughout that can be spruced up with either light touch ups or cleaning scuff marks off the walls, it’s a good idea to paint the primary living areas of the home, entryway and hallways. Not only will this make the home appear bigger, brighter and more welcoming, but the smell of fresh paint gives the sensation of a cleaner and newer home, much like new car smell. Plus neutral palates create more of a blank slate which will help future homeowners envision living there. Stick to lighter shades and endeavor to complement the color of the flooring. For instance you may be tempted to paint a cool grey tone throughout but if your carpet is a warm brown, stick to beige tones. DIY painting ranges from $200-400 per room or hire a professional painter for approximately $700 per room.

-

Clean or replace flooring- If you have outdated vinyl or dark, worn or stained carpeting, you may want to consider replacing it if a good steam clean doesn’t make it look somewhat new. Much like the smell of fresh paint, the smell of new carpeting is a trigger for people’s senses that a home is move in ready and is one less thing for them to worry about. Vinyl flooring has come a long way and laminates are inexpensive and emulate the look of hardwood. Be sure to once again stick with neutral colors and take into consideration the color of the walls when choosing flooring. This may be your biggest cost in prepping your home for sale but history has shown that homes which offer a flooring incentive vs. homes with new floors will languish on the market longer. Flooring expenses vary widely based off of cleaning vs. replacement costs, but the difference in the speed of how quickly your home sells may be well worth it.

-

Light it up- The easiest way to make your home appear inviting and ready for a new owner is to ensure every lamp and light in your home have working lightbulbs. This may seem insignificant but a chandelier with a blown light bulb can send a subliminal message that there may be other projects lurking around the house. You should also consider upgrading some of your light fixtures if they appear old or outdated, especially in the foyer, dining room, and bathrooms. Fairly affordable fixtures can be found at home supply stores or you can find used ones online or at thrift stores. If you prefer spending less money but perhaps more time, a couple of coats of bronze or black spray paint transform old brass light fixtures within hours and noticeably give the appearance of an updated feel. Light bulbs are inexpensive and changing light fixtures by either painting them or replacing them can range from $50 to several hundred dollars.

-

Turn it around- What is something that turns every day that you may not notice but a buyer will? Doorknobs, faucet fixtures and ceiling fans. Doorknobs are a fairly inexpensive and easy DIY project to update and faucet fixtures and ceiling fans can often be handled by the same handyman. If the style of any of these are outdated, much like light fixtures, your home will immediately appear newer with simple and somewhat affordable adjustments. For sources outside of home supply stores, Ebay is a great place to look for secondhand fixtures and Amazon has a wide selection of new products that are quite affordable. Prices start as low as $15 per doorknob, $50 per faucet fixture and $60 per fan plus any installation fees.

-

De-clutter, clean and stage- The majority of your investment here will probably be your time, some miscellaneous cleaning supplies and perhaps a short-term storage solution such as a family member’s garage or renting a POD. An empty room looks larger than a cluttered room and a well-staged, decluttered room looks larger than an empty room. Prepping your home for sale also means getting a jump on packing early. Remove all personal items such as family photos and memorabilia as possible so new buyers can picture themselves over the mantle, not your lovely family. De-clutter all countertops and organize storage to give the appearance of more than adequate space. Clean your home as if you were having an important guest come to dinner, and then clean it some more. And make sure it smells good. Obviously you can’t stop living your life, but understand if you cook inside and then show your home shortly after, the lingering smell of bacon grease or fish will be a turn off. Studies have shown the most appealing smells to be baking bread, cookies or vanilla. Air fresheners that neutralize odors are a solution as are plug ins if necessary (for instance in the kitchen or the room the dog sleeps in), but just be sure they are turned down low as too much fragrance can also backfire. And if you don’t have the money to hire a staging company ($300-$600 for initial consultation with no furniture rental), look online for ideas. Pinterest is a great resource for not just staging individual rooms but also outside spaces like decks and patios.

You’ve done a great job getting your home ready to sell, now what? Homes that are listed, marketed and sold by Realtors make more money and sell faster. According to the National Association of Realtor’s 2019 Profile of Home Buyer and Sellers, data shows that in 2019 FSBOs sold on average 40% less ($200,000 vs. $280,000) than homes listed by a Realtor. And it’s impossible to quantify the amount of time and headaches a Realtor can save you by handling the marketing, showing and contract negotiations required to get a home to closing, not to mention running interference for any challenges that pop up. After all your hard work, possibly the biggest return on your investment will be hiring a qualified and experienced Realtor.

By Holly Morris

For Additional Blog Content, Click Here!

10 of the Best Beach Towns to Retire

Thinking of retiring on the beach? Here are 10 of the best and most affordable options ranked by experts that looked at more than 1,300 towns with salty beach water. Limiting the choices to one per state, for variety, this ranking from a Realtor.com article is based on the population of residents aged 55 and over per capita, affordability based on the median list price, access to hospitals and other health care facilities, the number of amenities like golf courses (for low-impact exercise) and country clubs (for the social scene), as well as marinas and water-recreation businesses like boating and fishing, for that all-around beach town experience.

Thinking of retiring on the beach? Here are 10 of the best and most affordable options ranked by experts that looked at more than 1,300 towns with salty beach water. Limiting the choices to one per state, for variety, this ranking from a Realtor.com article is based on the population of residents aged 55 and over per capita, affordability based on the median list price, access to hospitals and other health care facilities, the number of amenities like golf courses (for low-impact exercise) and country clubs (for the social scene), as well as marinas and water-recreation businesses like boating and fishing, for that all-around beach town experience.

1. Murrells Inlet, SC – Median list price: $329,950

Just 15 minutes south of the bustling tourist shops, boardwalks, and mini-golf courses of Myrtle Beach, Murrells Inlet offers retirees a quiet respite from that popular vacation town. The former fishing village is bordered by a beautiful marsh shoreline and dotted with wooded areas. It also boasts a strong health care system, numerous golf courses, and a stunning sculpture park and wildlife preserve, Brookgreen Gardens, hailed as one of the Top 10 Gardens in the United States by TripAdvisor.

The mild weather, coastal scenery, good airport, and myriad amenities have made Murrells Inlet a desirable retirement destination for Northeasterners seeking a break from high tax rates and harsh winters.

Retirees can get into affordable homes starting at just under $200,000, including this $196,919 two-bedroom in a 55-plus community or this three-bedroom with a whirlpool hot tub—and no age restrictions—for $249,900.

“You kind of have the best of both worlds [in Murrells Inlet] if you’re looking for a nice, affordable area to retire to,” says Jeremy Jenks, vice president of sales at Keller Williams The Trembley Group. “It takes 15 minutes to get to everything Myrtle Beach has to offer without having to worry about traffic and stuff.”

2. Venice, FL – Median list price: $299,950

Venice’s shoreline is located halfway between Sarasota and Port Charlotte, on the eastern edge of the Gulf of Mexico. The powdery white-sand beaches are a paradise for sunbathers—or those who seek shade under an umbrella—and shell seekers. The city hails itself as “The Shark Tooth Capital of the World” due to the thick fossil beds that lie right under its gently lapping shores. The shallow and sedimentary conditions of the beach expose thousands of ancient shark teeth every day.

If hunting for shark teeth won’t keep the grandkids occupied, chances are nothing will—but you could always try taking them to the arboretum or Historic Venice Train Depot, or take them for a boat ride. Buyers can get into the market at a wide price range, from a three-bedroom manufactured home for $159,900 to this three-bedroom with water views and a private pool for $350,000.

3. Morehead City, NC – Median list price: $339,050

Morehead City has enough nautical attractions to make die-hard boaters keel over. The port town offers great boating, fishing, and nearly every type of water sport imaginable in both the sound and the Atlantic. Homes start in the $200,000 range, and it’s possible to snap up a townhome with an onsite dock such as this sprawling three-bedroom for $274,000 or this $350,000 three-bedroom with water views.

Though Morehead City is on the mainland, protected from storms by a barrier island, the city proper isn’t known for its beaches. To hit the soft sand of beautiful Atlantic Beach, locals have to drive about seven minutes across the bridge.

4. Lewes, DE – Median list price: $399,050

Lewes and nearby Rehoboth Beach have become one of the hottest LGBTQ retirement destinations on the East Coast. The welcoming area boasts many gay bars and restaurants, a thriving Pride parade (in years past), and an LGBTQ center—all on the shores of tax-friendly Delaware.

Historic Lewes has a more natural, small-town feel and (slightly) lower home prices. Retirees can get into active adult communities like Bay Crossing in a $239,000 two-bedroom condo all the way up to a fully kitted-out four-bedroom for $620,000.

“It’s a popular gay retirement community,” says Russell Stucki, real estate associate at Re/Max Realty Group. “People enjoy it.”

5. Toms River, NJ – Median list price: $279,950

New Jersey—and its infamous shore—gets a lot of flak, but it’s called the Garden State for good reason: It’s friggin’ beautiful when you exit the turnpike. That includes Toms River, a seaside town that’s nestled along the Atlantic Ocean and Barnegat Bay, a rich estuary that’s long been a destination for fishing, crabbing, and boating. The historic city boasts a vibrant downtown with shops and restaurants, 15 recreational parks (including a golf course), and waterfront views from both the mainland and the peninsula across the water.

Buyers looking for a deal can get into a one-bedroom home starting around $125,000 or even a four-bedroom right next to the water for $349,000.

6. Coos Bay, OR – Median home price: $279,050

Most folks probably don’t imagine spending their beachy retirement huddled up under layers of sweaters and blankets, but they’re missing out. The cliff-edged and chilly shoreline of Bastendorff Beach, just a short trip over the bridge from Coos Bay, is gorgeous, a wholly relaxing place to collect shells, pitch a tent, or ride a horse.

Many locals also take whale watching tours by boat, view masterpieces at Coos Art Museum, swing a 9-iron, or watch the pros play golf at the Bandon Dunes Resort, home to the Curtis Cup. Homeowners can look at the bay from their two-bedroom bungalow for just $169,000 or smell the salt air in a grand four-bedroom Dutch Colonial in the heart of town for a cool $649,000.

7. Seal Beach, CA – Median list price: $279,050

This is not a typo: Southern California does, in fact, boast affordable retirement homes right near the coast. Leisure World, a gated retirement community located just 12 minutes from the sands of Seal Beach, offers some serious deals. This renovated one-bedroom cottage is listed for just $199,999 and this two-bedroom at $225,000.

The large community has various purchase restrictions, including a minimum age, and in some cases requires all-cash transactions; but to buy in another part of the desirable beach town would cost at least $700,000. And locals are willing to fork over that kind of money for a reason. Seals actually do galumph around on the shore. The laid-back city boasts a restaurant- and shop-lined Main Street, which spills out to a nice pier and beach.

“Seal Beach is quaint and cute to walk around,” says Melinda Elmer, a Realtor® with Century 21 Masters. “It has a little bit of everything.”

8. New London, CT – Median list price: $207,950

Located at the mouth of the Thames River, this seaport city—the second-largest whaling port in the world back in the “Moby Dick” days—boasts a historic waterfront district that has become the creative hub of the city with art, music, and design venues, unique boutiques, and more than 30 restaurants. Retirees can take the grandkids on whale watching tours or picnic at one of the many parks or the beach.

However, what really makes this port town ideal for the 55-plus crowd is the easy access to quality health care. Part of Yale–New Haven Health, Lawrence + Memorial Hospital is home to the region’s only inpatient rehab unit and a nationally recognized cardiac rehabilitation program.

A two-bedroom condo right near the hospital and within walking distance to Ocean Beach can be had for just $99,000 and $209,900 can fetch a three-bedroom Cape Codder with a master bed and bath on the first floor, blocks from the water.

9. Rockport, TX – Median list price: $324,050

This Gulf Coast tourist haven has clean beaches, great fishing, and fantastic fowl. It has 10 birding sites on the Great Texas Birding Trail and the planet’s sole migrating flock of over 265 whooping cranes, which passes through the Aransas Wildlife Refuge every winter.

About 27% of the city’s 10,000 residents are aged 65 and up. Many of them seek out single-story homes with attached garages right around the golf course, marina, and beaches. They include this three-bedroom on the water for $275,000 and this two-bedroom cottage for $219,000.

10. Hyannis, MA – Median list price: $399,950

With its bustling main street, John F. Kennedy Hyannis Museum, and world-renowned Cape Cod Hospital, Hyannis is basically the hub of the Cape. It’s home to lots of shopping, plenty of restaurants, nice golf courses, a great sailing scene, and beautiful beaches. It even has an airport and ferry terminal that connects the mainland to Martha’s Vineyard and Nantucket.

Many of the retired residents of Hyannis move into their former summer homes, but there are still plenty of boomers relocating to the area. Year-round homes start around $350,000 and reach nearly $4 million. Though a four-bedroom on the beach will set you back $1,650,000, a two-bedroom right next to downtown can be purchased for just $249,900.

“There’s still a lot of areas in Hyannis that are very affordable,” says Jeanette Neeven, a Realtor with Century 21 Cobb Real Estate. “Obviously, just like anywhere, the closer to the water you are, the more expensive the property.”

Thank you www.realtor.com for this article. For other great articles, Click Here.

For Additional Blog Content, Click Here!